Mar 27, 2026

Eurex

Credit Index Futures pass first volatility test as volumes build

By Davide Masi, Global Product Lead for Credit, Eurex

The recent volatility shock that hit markets at the beginning of March constituted the first true test of a product that has built steady momentum in recent years – Eurex Credit Index Futures.

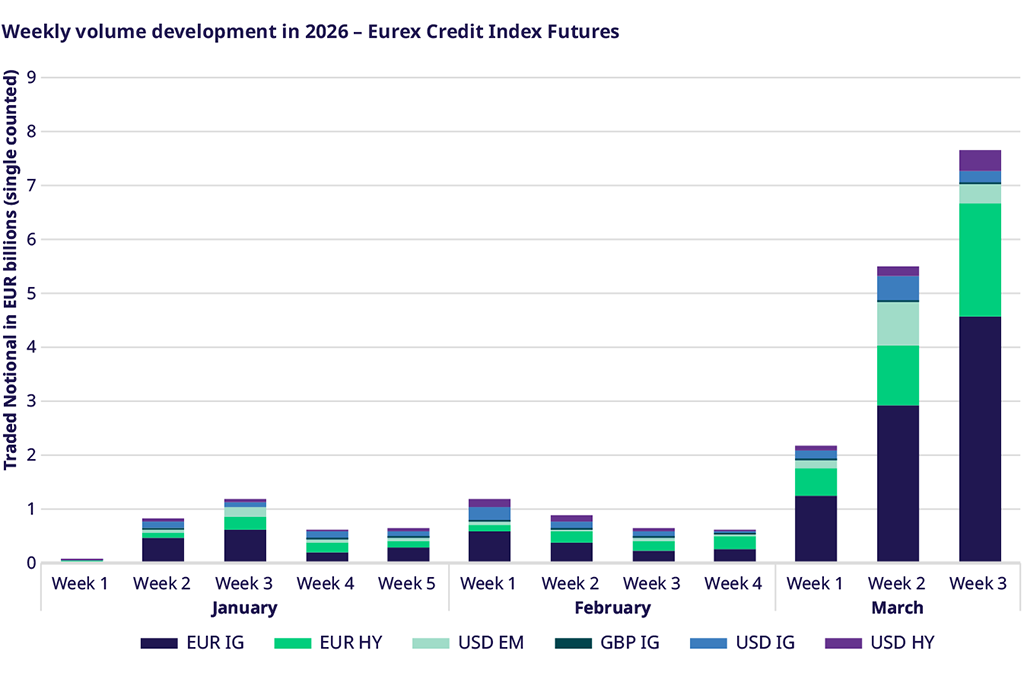

March 2026 volumes ahead of the roll in Eurex’s Euro IG (LXYA) and Euro HY (AHWA) index futures had already exceeded their February levels.

More than 10,000 lots were traded in LXYA (about EUR 1.9bn in notional) and about 15,000 lots were traded in AHWA (about EUR 900m in notional) over the first ten days of March. These volumes almost entirely consisted of outright risk trades, not rolls. Activity approached, and at times even surpassed, trading levels of more established macro credit trading instruments, such as Total Return Swaps and Fixed Income ETFs.

When adding rolls from expiring March contracts to June 2026 positions, Eurex hit record trading day activity on March 13, with 49,254 lots traded across the Credit Index Futures product suite.

This significant rise in volumes not only speaks to the inherent attraction of Credit Index Futures as a risk instrument in volatile conditions, but also to the years of careful work that have gone into building the foundations for the market.

Thorough engagement with the dealer community has ensured that they were ready and eager to price their clients’ futures trades as volatility began. Similarly, Eurex’s work with buy-side firms during 2024 and 2025, to fully explain the product and integrate it into risk-management and portfolio-management platforms and workflows, meant that these participants were fully comfortable with the futures product ahead of the shock.

All of these efforts prepared market participants to not only absorb the initial outbreak of volatility, but also the surge in trading activity that came after it. Repositioning by large fast money accounts, as well as the rapid repricing of credit and rates conditions that have all taken place in recent weeks, all served as a firm test of the market’s resilience. Beforehand, it was an open question as to whether Credit Index Futures could prove themselves as an alternative product for exchanging risk in the credit trading ecosystem, or prove inadequate to the challenge and fall short under their first major volatility shock.

Buy-side clients were able to transact in the market for large sized trades and at tight bid/offer spreads. Order book spreads in LXYA contracts were about 10bps at the beginning of March and have since tightened to 5bps. AHWA spreads behaved similarly, with only about 5-10bps of widening. Trading was generally in line with market movements in the iTraxx Crossover and Main CDS indices.

Market participants have significantly maintained and increased open interest beyond the first ten days of March. During previous smaller and more isolated episodes of volatility, clients that are very active in Credit Index Futures have tended to close their positions out of fear that volatility will harm liquidity conditions.

During this larger market shock, most closing of positions was swiftly followed by the opening of new ones, as market participants changed from long to short positions, ultimately driving an increase in open interest as users moved to build hedges against potential future volatility spikes and market sell-offs.

Block trades, a foundation of the market, have also seen a surge in activity, with 27 executed in LXYA and 40 in AHWA as of 13 March, 2026. Around 40% of LXYA block trades have traded at less than 2.5bps from mid during March, with another 30% at less than 5bps from mid. Meanwhile, about 60% of block trades in AHWA contracts traded at less than 5bps from mid.

Rising activity has not been constrained to the core LXYA and AHWA products, with USD EM index futures (XZSA) also building significant momentum this year. Notional outstanding has already exceeded USD 600 million, while trading is around USD 800 million in notional.

Geopolitical tensions are likely to continue shaping market trajectories, keeping the outlook highly uncertain. Risk management and finding the right instruments to achieve it are more important than ever for market participants. For those active in credit markets, futures can now be safely counted as part of the toolbox for navigating the uncertain times ahead.