Jun 12, 2026

Eurex | Eurex Repo | Eurex Clearing

Eurex is paving the way for future cross-margining between repos and derivatives

The appeal of European cross-margining is easy to understand but hard to implement. Eurex is introducing bond portfolio margining for the first time by extending its established PRISMA risk model, providing a new opportunity for dealers to reduce costs for cleared products and setting the scene for a future cross-margining between repos and derivatives.

The execution of cross-margining, one-pot margining or cross-product margining has been live for years in various forms. Various fixed income derivatives such as futures and swaps, and equity index futures and options, can be analyzed together in risk models to reduce the amount of collateral that dealers need to post to central counterparties (CCPs) on behalf of proprietary and client trading. Dealers can conduct more business if they need to post less margin, resulting in larger revenues. Every active trading firm is aware of their margin requirements with CCPs either real-time or end of day; reducing this cost creates direct front-office opportunities.

The ability of a CCP to run a well-calibrated risk model is a central tenet of financial market infrastructures; it is one of the most important things that CCPs do and is a primary focus of regulatory oversight. The CPSS/IOSCO Principles for Financial Market Infrastructures state that “A CCP should adopt initial margin models and parameters that are risk-based and generate margin requirements sufficient to cover its potential future exposure to participants in the interval between the last margin collection and the close out of positions following a participant default.”1 Getting the risk model right is the first order of business for a CCP.

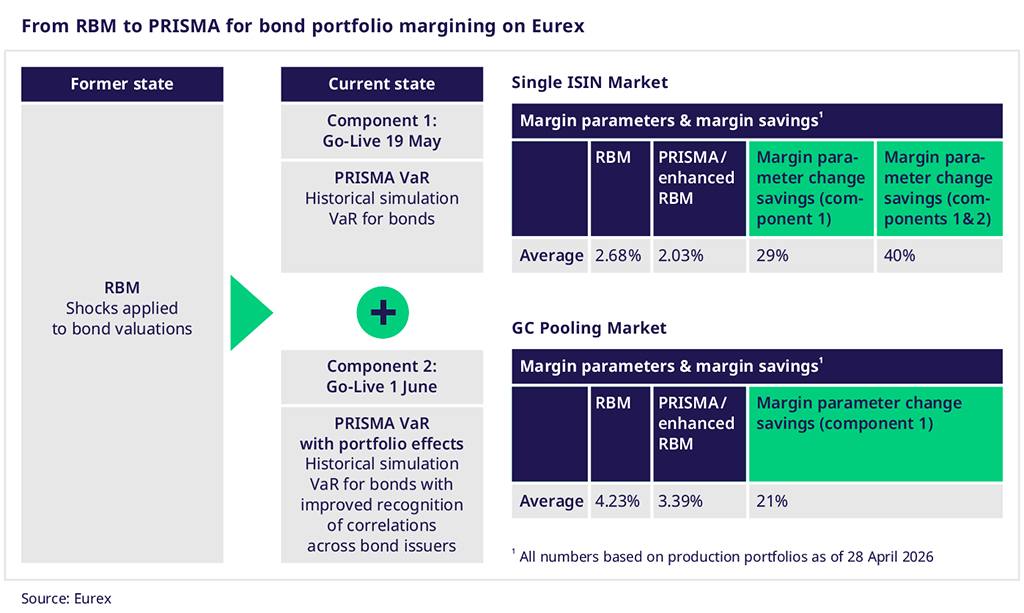

The margin innovation now being introduced by Eurex is to align the methodology of bonds with that of Exchange Traded Derivatives (ETDs) and OTC interest rate swaps (IRS). This is a migration from the current Risk Based Margin Methodology (RBM) to the established Portfolio-based Risk and Margin system (PRISMA). In a first step, this will introduce a superior calibration of margin parameters (≈haircuts) of the more than 14,000 securities eligible for repo trading & clearing at Eurex. From June 2026, Clearing Members can additionally elect to margin the most commonly used securities in European specific ISIN repo transactions, a universe of roughly 1,500 securities, under the PRISMA methodology and benefit from enhanced bond portfolio margin offsets. Both measures will reduce the cost of centrally cleared repos at Eurex and is expected to boost repo trading activity and liquidity.

Why PRISMA matters

PRISMA is Eurex’s proprietary risk margin calculation engine. Launched in 2013, the model assesses market volatility as a core consideration and adjusts margins accordingly. Margins decrease as volatility decreases but not too low as to lack protections for dealers, clients and the CCP itself.

PRISMA sets margin levels by focusing on Liquidation Groups within customer and proprietary positions for the markets and venues cleared by Eurex Clearing. Prisma calculates portfolio margining for Liquidity Groups with the same holding periods: for example, if a dealer holds a EURO STOXX 50® Index and the same DAX® Futures, these products can be looked at together for risk exposure purposes. Or, cross-margining can be calculated across OTC IRS and listed money market and fixed income futures.

Equivalent risks and exposures are treated in the same category, allowing dealers to consolidate their margin requirement into one aggregated view rather than having to post margin for each individual transaction. By estimating the actual liquidation and worst-case losses of any portfolio in a Liquidation Group, PRISMA then determines the correct margin for the portfolio.

PRISMA and cross-margining offer dealers and clients a cost advantage in the market by calibrating the actual margin requirement to their specific portfolio and cross-product volatilities. Hedge funds in particular have been eager to take advantage of cross-margining opportunities both in general and on Eurex specifically. The better these sophisticated risk models assess exposures, the more adequate risk is margined. This is of major importance to many clients, in particular, hedge funds employing relative values strategies.

Running the numbers: the value of migrating to PRISMA

Eurex analysis shows that the main savings from the integration of PRISMA bond portfolio margining will be in the single ISIN repo market. The current bond margin methodology, RBM, is predominantly assessing individual shocks to bond valuations when evaluating collateral requirements. As the shift to PRISMA happens, Eurex will use a Value-at-Risk (VaR) model to run historical simulations on actual bond movements and capture risk correlations between bond issuers on a bond portfolio basis (see exhibit).

Compared to the previously used RBM methodogly, the average margin improvement in PRISMA based on production portfolios of specific ISIN repos is approximately 40%, with some members benefiting by up to 82%. There is less benefit in the GC Pooling market as repo portfolio effects are not considered initially. However, the enhanced re-calibration of bond margin requirements still generate margin savings of around 21%.

Another important difference is that RBM historically has seen a twice a year recalibration of parameters for margin calculation. Since 18 May 2026, margin parameters are now recalibrated on a daily basis. By dynamically reassessing the risk factors behind individual bond securities, Eurex Clearing can more accurately determine what the right margin requirement should be. This is a large contributor to the margin savings that Eurex has found in its impact analyses.

What’s next for cross-margining on Eurex?

Adding further bond markets to PRISMA will continue: we recently started the regulatory approval process to offer cross margining between repo, money market and bond futures as well as OTC IRS.

Incorporating more product sets into PRISMA will be a contributing factor in reducing repo dealer balance sheet costs and supporting an increase in client business facilitation. Margin offsets are equally a significant part of a wider strategic push to make Eurex cleared repos more attractive to non-bank financial institutions (NBFIs).

Another development is an extension of repo settlement options in order to facilitate netting and improve intraday liquidity management. This is expected to become increasingly relevant with the move to T+1 bond settlement.

Eurex clients with a Clearstream Europe AG (formerly Clearstream Banking Frankfurt) settlement account and a cash account at their domestic central bank can now settle repo transactions of all major European bond markets in central bank money (CeBM) at a single CSD. Moving to CeBM and away from commercial bank money can improve liquidity, eliminate settlement credit lines and reduce risk. This single settlement model reduces operational risk and can reduce the regulatory capital costs of the repo business. Adoption has been rapid across the Eurex customer base.

Integrating repo transactions into PRISMA marks a major milestone for European market infrastructure. By enabling eventually cross-margining across fixed income securities and derivatives, Eurex is helping clients unlock capital efficiencies and streamline their risk management. Equally, supporting a consolidation of repo settlement at a single location allows participants to reduce operational risk and improve intraday liquidity management.

By Frank Odendall, Head of Funding & Financing Products & Markets, Eurex

This article was first published on Finadium on 11 June 2026

____________________

1 “Principles for Financial Market Infrastructures,” Committee on Payment and Settlement Systems and the Technical Committee of the International Organization of Securities Commissions,” April 2012, available at https://www.bis.org/cpmi/publ/d101a.pdf