Apr 23, 2026

Eurex

Global exposure and regional leverage: U.S. equity total return futures for European and Asian investors

Total Return Futures (TRFs), the futurized version of total return swaps (TRS), are used by banks and leveraged investors looking for exposure and hedging opportunities. Demand for equity TRFs on U.S. underlyings at Eurex warrants closer examination to understand who is interested, why, and how the ecosystem is developing to support efficient, cleared financing products.

Index and basket TRFs based on U.S. equities, traded in Europe for non‑U.S. investors, meet a growing need for investment strategies in this large asset class. TRFs are becoming a mainstream leveraged trading product across multiple geographies. They are also part of the market’s evolving use of cleared products to support financing requirements across a broad range of instruments.

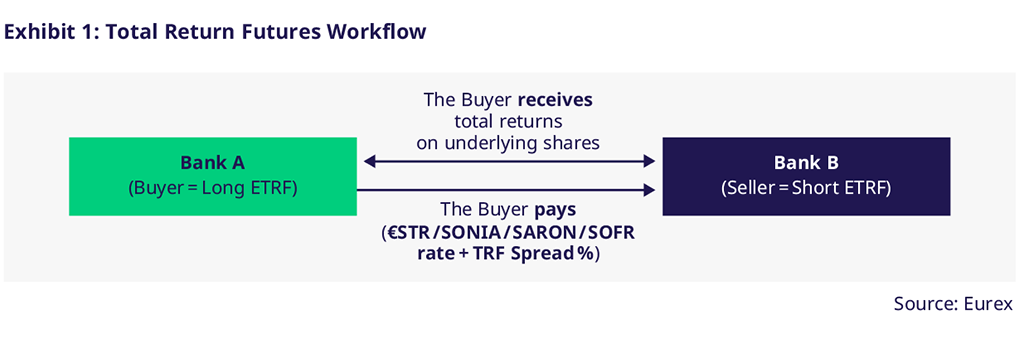

Equity Total Return Futures (ETRFs) are listed futures contracts used as building blocks for bespoke baskets (BTRFs) constructed by traders seeking to replicate an over‑the‑counter equity basket TRS, which is itself a substitute for a securities loan for short sales or margin borrowing for long positions. The buyer (long) receives the total returns on the underlying shares and pays a financing amount on the notional based on an agreed rate (see Exhibit 1). Alternatively, the buyer can take a short position to gain exposure to the opposite market direction.

BTRF users are attracted to balance sheet efficiencies, standardized terms, and transparent pricing. For many dealers, BTRFs are now part of a broader toolkit of baskets, synthetics, and dividend products across the equity index product landscape, supporting flow trading, proprietary trading, inventory management, and financing.

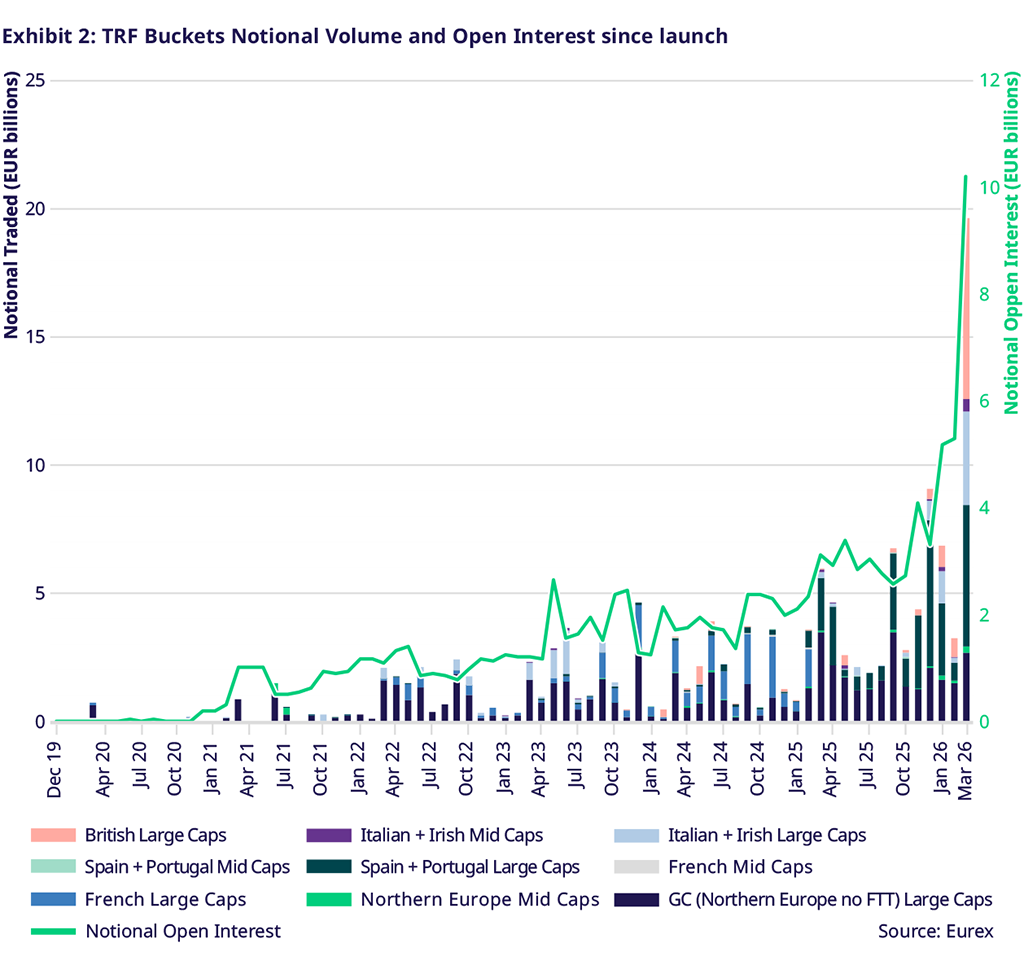

Overall, the Eurex ETRF/BTRF offering has a broad scope, with four currencies (EUR, GBX, CHF, and USD) across 465 ETRF products. This includes the February 2026 listing of 73 U.S. names based on the STOXX® USA 50 benchmark. Market interest in BTRFs has increased significantly: notional open interest across EUR‑denominated TRFs exceeded EUR 5 billion at the end of 2025, nearly doubling year‑on‑year (see Exhibit 2). Open interest across all ETRFs (including UK names) exceeded EUR 10 billion in notional terms as of March 2026. In Q1 2026 alone, record volumes were traded – nearly EUR 30 billion notional (+188% year‑on‑year), with over EUR 140 billion notional traded cumulatively since launch.

Across all products, the advantages of TRFs over TRS may include more liquid markets, the reduced counterparty risk of a cleared product, and lower margin requirements versus bilateral trades under uncleared margin rules (UMR). Dealers can create netting sets on central counterparties (CCPs) that drive down margin costs by offsetting positions for the same product or across multiple types of cleared equity derivatives. Ease of substitutions in basket TRFs can provide flexibility to banks in meeting client trading requests, managing inventory and internalizing order flow.

A new mix of clients are participating in TRFs including traditional asset managers, multi-strategy hedge funds, relative value hedge funds and index arbitrage traders. Market volatility in 2025 and geopolitical turmoil in 2026 contributed to drive growth and dealers noted a bigger desire for leverage among clients than in previous years. Buy side firms can see the margin benefits from TRF compared to the equivalent OTC derivative TRS and, where possible, have moved in the TRF direction.

TRFs lend themselves to specialization, whether as a customizable basket or based on the underlying securities or bonds of different jurisdictions. The common theme is market demand, and will there be enough liquidity for clients, dealers and the clearing firm to successfully build momentum. In this context, USD-based TRFs on U.S. equities are an unusual case with built-in demand.

Global demand for financing U.S. equities

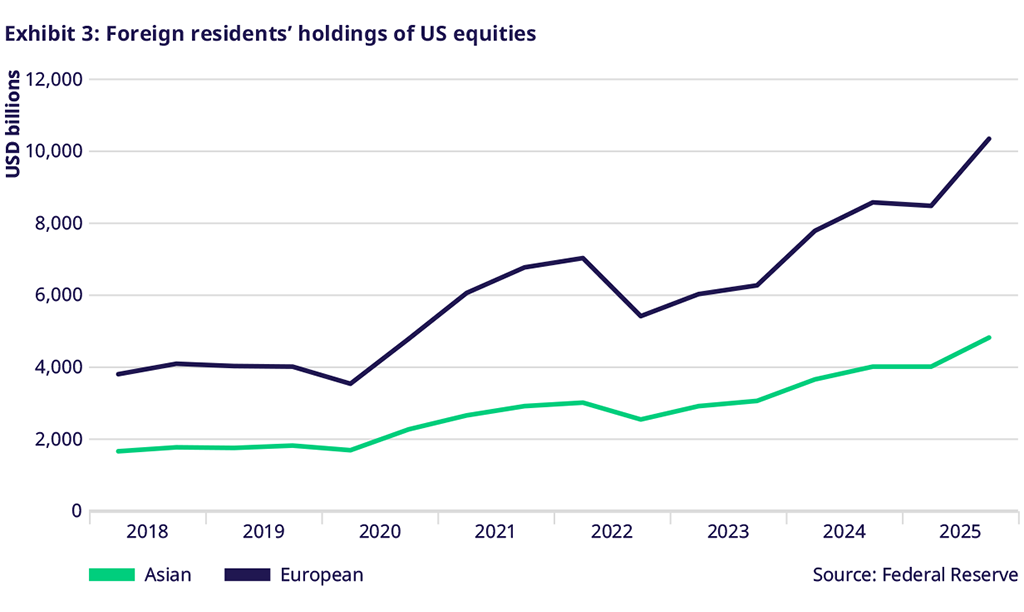

U.S. equities hold a particularly strong attraction for global asset managers. Data from the Federal Reserve show that the dollar value of European holdings of U.S. equities has risen sharply in recent years, driven by an equally strong surge in the U.S. equity market (see Exhibit 3)1. European stock holdings are now above USD 10 trillion and increased by 20% from 2024 to 2025. Asian investors have also increased their holdings, but more gradually in total dollar terms: they now hold just under USD 5 trillion, up from USD 4 trillion in the previous year.

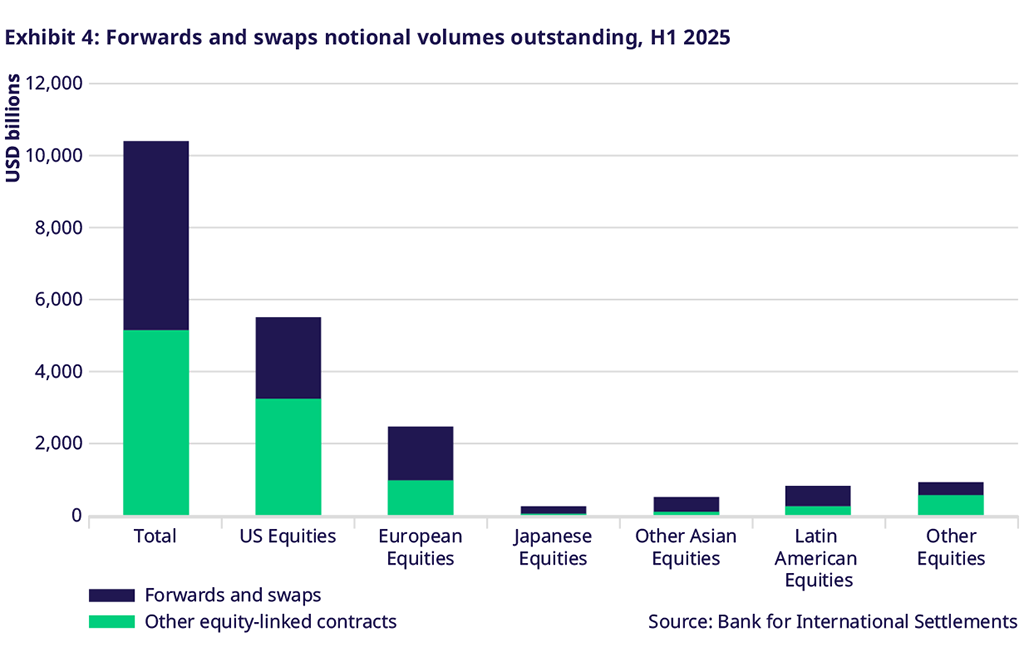

Leveraged trading strategies globally are likely to come into contact with the U.S. derivatives market over time, whether for hedging existing positions or seeking leverage to support an investment thesis. The Bank for International Settlements (BIS) reports that forwards and swaps volumes for U.S. equities totalled USD 2.2 trillion in the first half of 2025, significantly higher than the USD 1.5 trillion in European equities and USD 383 billion in Asian equities (see Exhibit 4)2. The U.S. futures and swaps market is also larger than markets for other U.S. equity‑linked contracts.

Prime brokers supporting European and Asian investors report that they have invested heavily in derivatives, including total return swaps and futures, in an effort to better serve their clients; as a result, they see this demand first-hand. Finadium research shows that well over half of equity prime brokerage revenues now come from synthetic products3. Growth in swaps and futures activity requires prime brokers, in turn, to focus on financial resource management and balance sheet capacity, which can be consumed more easily by bilateral trading activity than by cleared business. This dynamic helps shift dealer interest towards cleared TRF products.

Eurex has found that regional preferences have shifted when it comes to TRFs. While global volumes in S&P 500 TRFs have grown rapidly, European markets continue to retain key advantages in liquidity, bid‑offer spreads, and the maturity of products and infrastructure. Today, Europe remains the preferred venue for directional funding trades, while the U.S. is attracting increasing interest in relative‑value and diversification strategies.

Stuart Heath, Product R&D, Equity and Index at Eurex, highlighted the range of market requirements addressed by the new Eurex ETRFs on U.S. equities:

European and Asian clients have large positions in U.S. equities that require the same hedging and leverage opportunities as U.S. clients. Eurex USD ETRFs provide this exposure to these firms, while delivering the full range of clearing and netting benefits for clearing banks.

IRS Section 871(m) compliance

From a tax perspective, non‑U.S. investors in U.S. equity derivatives are impacted by IRS Section 871(m), which applies a 30% withholding tax to dividend equivalent payments that replicate the effect of a dividend. This measure is intended to prevent non‑U.S. investors from sidestepping U.S. dividend withholding taxes by using equity derivative structures. While currently limited to delta‑one instruments, Section 871(m) will expand from 1 January, 2027, to cover transactions with a delta of 0.8 or higher. Multiple offsetting positions will be in scope, so firms must determine whether they have a combined delta of 0.8 or more.

Eurex’s USD‑denominated ETRFs are a delta‑one product and will therefore be in scope for Section 871(m). However, the structure of Eurex ETRFs passes through only the net dividend amount (i.e. with the 30% withholding tax applied). It is expected that traders will position out of an ETRF in a basket prior to the underlying stock’s ex‑date. Eurex sees similar behaviour in the EUR‑denominated TRF products.

U.S. equity TRFs in the context of a European growth ecosystem

Investing is global, but infrastructure and markets provide products to regional, regulated audiences. While European and Asian investors may be leveraged in U.S. equities, they must also trade with banks that are approved by their regulators and on exchanges that can offer appropriate solutions. Likewise, banks and brokers may face global challenges but seek to solve them both regionally and locally. In both cases, USD-based equity TRFs traded in Europe for non‑U.S. investors meet a specific need.

The launch of USD ETRFs is progressing in parallel with other advances in the TRF trading and technology ecosystem. In 2025, Wematch.live announced support for Eurex’s Basket TRFs on the Wematch platform. This development complements the technology firm’s trading and workflow services to global banks in total return swaps. The ability to compare pricing and potential balance sheet implications side by side, and then communicate the impact to clients, can be a significant advantage for the dealer community. Integration with other order management systems and post‑trade solutions can further enhance operational efficiency by automating lifecycle management, reconciliation, and regulatory reporting. Together, the growth of the ecosystem lowers barriers to entry, reduces operational complexity, and helps firms manage risk.

Eurex’s USD‑denominated ETRF and BTRF products are an important step in the ongoing evolution of the TRF market. They enable the large volume of financial activity in Europe and Asia to access USD synthetic exposure with greater transparency, scalability, and capital efficiency than over‑the‑counter alternatives. For dealers, further expansion of USD ETRFs creates additional options for balance sheet savings, while reducing operational complexity and delivering potential margin efficiencies.

By Josh Galper, Managing Principal, Finadium

This article was developed in collaboration with Finadium.

_________________

1 "Foreign Residents' Holdings of U.S. Long-term Securities by Security Type,", Federal Reserve, available at

https://www.federalreserve.gov/releases/efa/international-portfolio-investment-figure3.htm

2 "Equity-linked derivatives", Bank for International Settlements, available at

https://data.bis.org/topics/OTC_DER/tables-and-dashboards/BIS,DER_D8,1.0

3 "Prime Brokerage Equity Finance Revenues in 2025", Finadium, August 2025, available at

https://finadium.com/finadium-report-desc/prime-brokerage-equity-finance-revenues-in-2025/