Apr 22, 2026

Eurex

Q1 2026 Market Review: Long-term Interest Rates

Q1 markets were driven by geopolitical shocks and renewed inflation concerns

Global financial markets in the first quarter of 2026 were dominated by, a challenging macroeconomic backdrop shaped by geopolitical tensions and a renewed cycle of inflation concerns. Q1 2026 and mainly March 2026 proved to be a turning point, as investors were forced to reassess expectations for monetary easing amid escalating global risks.

Geopolitical conflict triggers energy and inflation shock

The dominant driver of market dynamics in Q1 2026 was the escalating conflict in the Middle East, which evolved into a global energy supply shock by March. Disruptions to energy markets reignited inflation concerns across all economies, reversing the disinflation narrative that had gained traction at the end of last year.

This renewed inflation pressure triggered a sharp sell-off in global bond markets. Bond yields moved higher across the curve as investors adjusted inflation expectations and questioned the timing and extent of future interest rate cuts.

Central banks hold steady markets reprice expectations

Against this backdrop, both the Federal Reserve and the European Central Bank opted to keep policy rates unchanged. The Fed held rates at 3.75 percent, while the ECB maintained its policy rate at 2.15 percent. Despite heightened volatility, the ECB noted that inflation remained in a "good place", signaling confidence in the underlying disinflation trend prior to the energy shock.

However, markets adjusted rapidly. While expectations for Federal Reserve rate cuts had been priced earlier in the quarter, the inflationary implications of the Middle East conflict led investors to reassess that outlook. In contrast, markets began pricing in potential rate hikes from the ECB, reflecting diverging policy expectations between the two central banks.

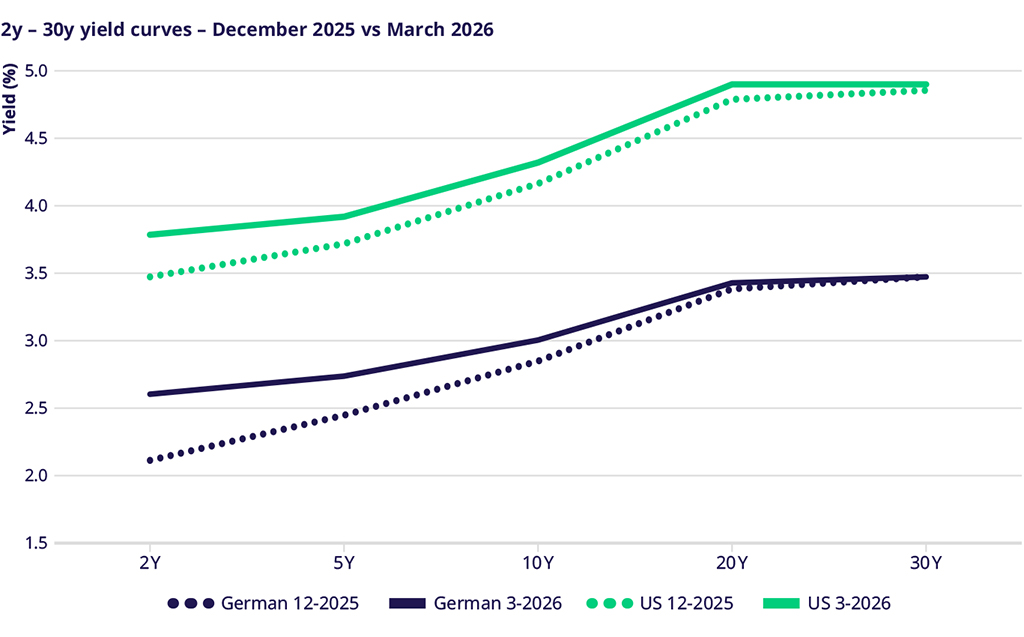

Bond yields rise across the curve

Bond markets reacted decisively to the renewed inflation narrative. German Bund yields and U.S. Treasury yields rose across the curve, driven by heightened geopolitical risk and concerns over sustained price pressures. The sell-off underscored the sensitivity of fixed income markets to energy-driven inflation shocks and reinforced the importance of geopolitical risk as a macro variable.

Yield curve dynamics reflected these shifts. The 2s10s spread stood at 53 basis points in the United States and 40 basis points in Germany, highlighting a steeper curve as long-term yields moved higher relative to short-term rates.

Peripheral spreads continue to tighten

Despite broader market volatility, euro area peripheral spreads showed resilience. The 10-year BTP vs Bund spread narrowed further, declining to 90 basis points. This tightening suggests continued investor confidence in Italian sovereign debt and reflects strong demand for yield in a higher-rate environment, even as core yields rise.

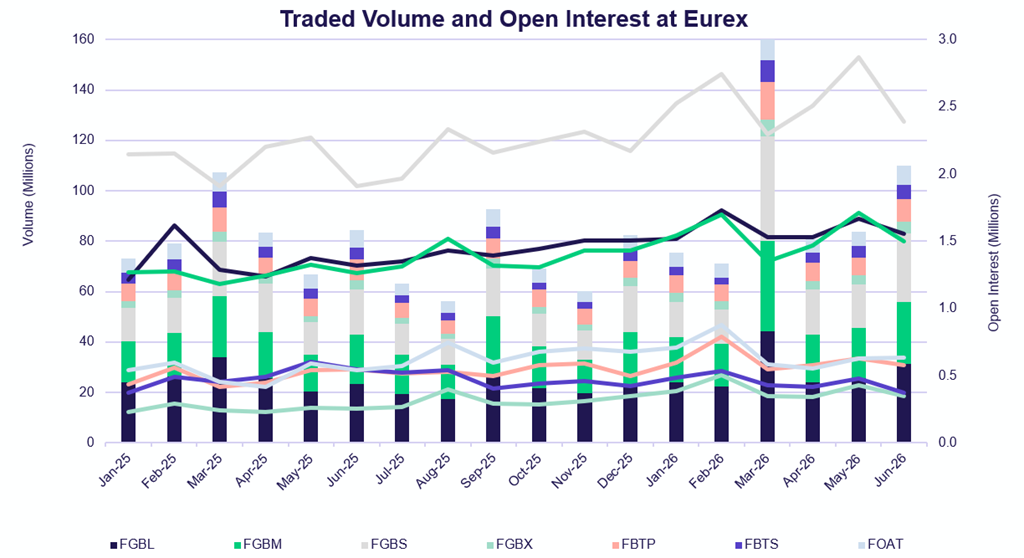

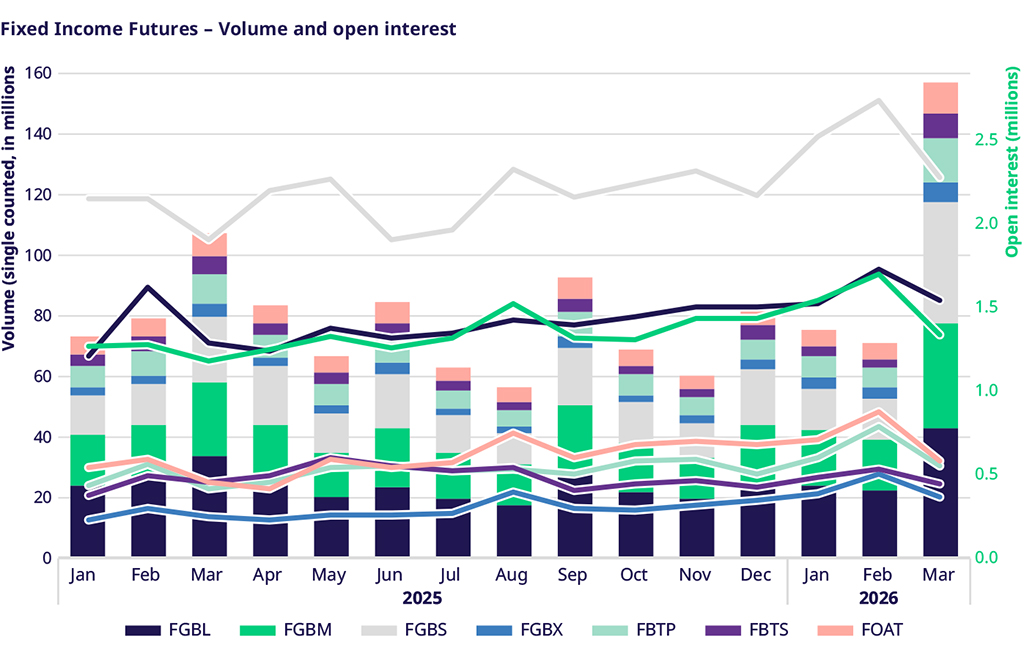

Rising volatility drives trade size and trading activity in Bund, Bobl, and Schatz

Average trade sizes in Euro-Bund Futures (FGBL), Euro-Bobl Futures (FGBM), and Euro-Schatz Futures (FGBS) stood at 22, 38, and 53 lots, respectively, over the quarter. On a quarter-on-quarter basis, trade sizes were broadly stable, with FGBL and FGBS unchanged and FGBM declining modestly by 6 percent. The resilience in trade sizes highlights sustained market participation despite heightened volatility.

Trading across all tenors was strongly supported by rising yields along the entire curve, as investors repositioned in response to renewed inflation concerns. Median trade sizes for FGBL and FGBM were approximately 4 and 7 lots, respectively, while FGBS trade sizes fluctuated more widely, ranging from 1 to 10 lots. This dispersion reflects a mix of tactical positioning and risk management activity amid rapidly shifting macro conditions.

Trading activity strengthened further in Q1, supported by increased volumes and rising open interest across major rates futures. Eurex volumes rose 18 percent year-on-year across the core long‑term interest rate (LTIR) futures segment. Open interest growth was particularly strong in the German and Italian markets, increasing by 20 percent and 31 percent respectively, while French contracts saw a 27 percent year-on-year increase. Meanwhile, Italian contracts (BTP/BTS) also recorded robust volume growth, underscoring sustained investor engagement amid elevated volatility. Short-end BTS contracts saw open interest decline by 2 percent year-on-year, however, pointing to a rotation toward longer-duration exposure amid elevated volatility.

At the top-of-book level, market depth reached record levels during the quarter. Best bid and offer (BBO) sizes in Bund futures accelerated steadily, peaking at over 1,000 lots, reflecting strong liquidity provision and increased electronic participation. However, this improvement was temporarily disrupted during the Q1 contract roll and periods of heightened geopolitical tension. During these episodes, liquidity conditions tightened noticeably, with top-of-book sizes falling to lows of approximately 190 lots. Elevated risk levels led liquidity providers to adopt a more cautious stance, refraining from immediately replenishing BBO sizes to typical levels.

Despite these fluctuations, liquidity remained resilient and executable. Eurex's posted liquidity continued to translate effectively into tradable depth. Under normal market conditions, the median trade impacted the relevant FGBL BBO side by an average of 1.2 percent. During the roll period and as the Iran conflict escalated, trade impact increased to a still-manageable 3.5 percent, highlighting the market’s ability to absorb risk even amid periods of intensified volatility.

Outlook

Looking ahead, markets remain highly sensitive to developments in geopolitics and energy supply. Inflation dynamics, rather than growth concerns, have reasserted themselves as the dominant driver of monetary policy expectations. While central banks maintain a cautious stance, the Q1 experience highlights how quickly the policy outlook can shift in response to external shocks.

As investors navigate the coming quarters, volatility is likely to remain elevated, with bond markets particularly exposed to changes in inflation expectations and geopolitical risk.