Aug 17, 2023

Eurex

FIC Credit Market Snapshot July 2023

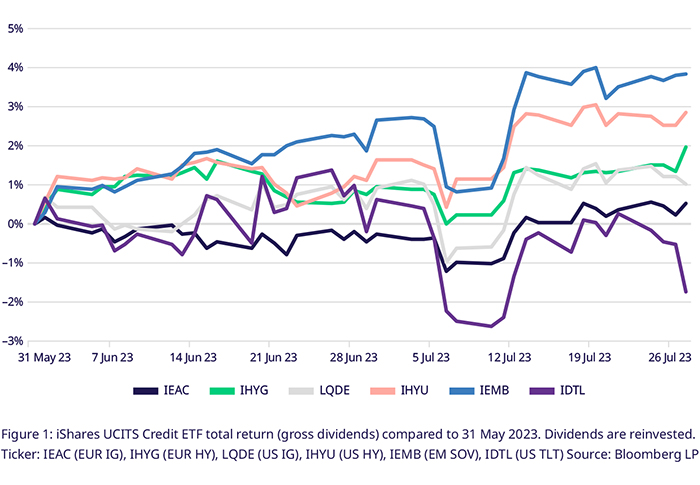

Risk-on-Rally fuels Credit spread compression

Resolution of Debt Ceiling negotiation and soft-landing hopes fuel rally in US names, higher risk tranches. IEMB + 4.52%, IHYU + 2.95%

USD and EUR-denominated names saw positive returns throughout June as the uncertainty around the debt ceiling discussion subsided. Both IHYU (USD High Yield) and LQDE (USD Investment Grade) outperformed their European counterparts IHYG (EUR HY) and IEAC (EUR IG). The iShares J.P. Morgan USD EM Bond UCITS ETF (IEMB, EM SOV) performed the best over the month, with a total return approaching 3%. Yield curves rising at the beginning of July led to some losses, especially in USD UCITS ETFs with a longer duration and time to maturity, like IEMB, LQDE and IDTL (20yrs+ Treasuries). All tickers above, except IDTL, were able to recoup the losses towards the end of the month. IEMB performed best from a total return perspective, with gains of 4.52%, including dividends (net), followed by the High Yield ETFs IHYU and IHYG at +2.95%, 1.77%.

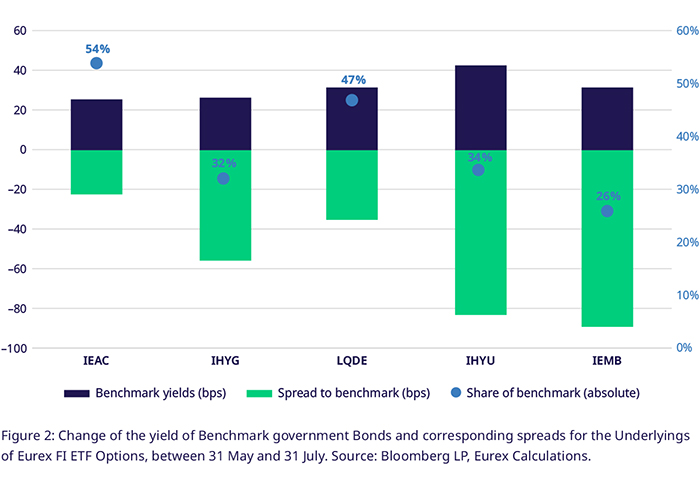

Spreads compressing (IEMB -89bps, IHYU -83bps), YTM carry drive returns. Yield curves rose over June and July

Although benchmark yield curves in Europe and the US continued to climb, the hope for a soft-landing drove compression in credit spreads. This, and high yields embedded in the ETFs’ holdings, drove returns, especially in the higher risk tranches. IEMB saw spreads compress 89bps, more than offsetting a 32bps rise in the US 10yr Treasury yield. The High Yield ETFs IHYU and IHYG saw credit risk expectations reduce similarly, as the USD name had its spread to benchmark contract 83bps while the other shed 55bps. Investment Grade credit ETFs favored by investors mulling a hard landing saw less contraction that could at least offset the rising yield curves.

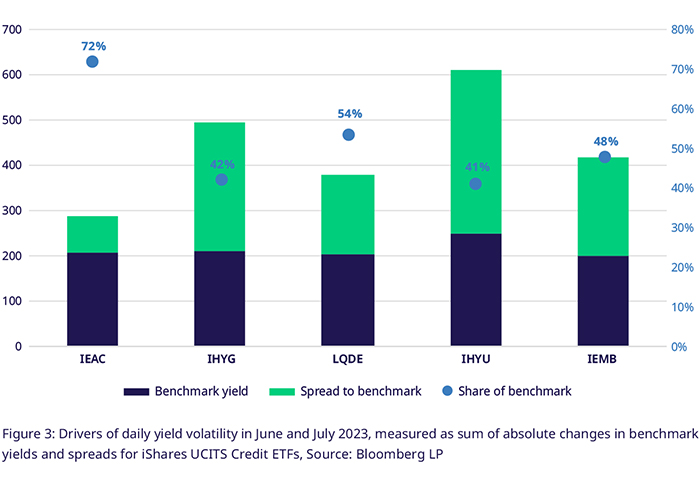

USD High Yield daily volatility dominated by spreads. However, month-on-month returns dominated by short end benchmark rates, more volatile than longer end

For IHYU, credit spreads accounted for 56% of daily yield movement totaling 294bps. Secondly, we observe the movement over the whole month and gauge the impact of both components over a longer period. When taking the longer horizon, benchmark yields continue to make up more than half the yield movement, as they have since mid-2022. Over the whole month, spreads widened by 22bps, while benchmark yields rose by 27bps.

Credit spreads follow global risk appetite, IEAC still moderately cheap vs. 5yr average, LQDE richest

The average credit spreads of EUR Investment Grade Corporate Bonds in IEAC are still slightly cheap compared to the historical average of the last 5 years, even after months of compressing spreads. The spread to bench was 0.35 standard deviation above its 5yr historical average, including the low-yield pre-covid area and the crises of recent years. This indicates some more room for further spread compression should bullish sentiment persist. IHYG was almost spot on the 5yr average, while all USD credit ETF Options underlyings ended the month with spreads trading slightly rich, led by LQDE at -0.72 standard deviations below the historical average.

Higher risk names in EUR, US promise high yields with low duration, with EUR High Yield volatility lower than EUR IGBreakevens, which is the yield to maturity (YTM) over duration, measure the amount YTM can move before total return becomes negative. Generally, higher risk corporate bonds have a shorter duration and higher yields, pushing up breakevens. Unsurprisingly, IHYG breakevens ended July as the highest out of the observed at 2.56, meaning a 250bps+ move in yields would be necessary for total return to be negative. Duration decreases with rising yields and we see all ETFs’ breakevens at least one standard deviation above the historical average. Higher yields baked into bond prices are usually justified by higher volatility expectations. However, 90-Day volatility of IHYG was actually lower (4.56 vs 5.21) than for IEAC, which led to IHYG having the highest breakeven per unit of volatility at 55.

Benchmark yields drive volatility in IG names, HY, EM driven by credit risk

European benchmark yields moved similarly, both on the long and short end. But, IG credit spreads were stable, which led to 72% of total yield movements of bonds in IEAC being explained by the Benchmark government bond yield. In the US, the short end was more volatile than the long end, which, in turn, was as volatile as the European counterpart. However, credit spreads did experience significant movement as well, leading to only 53% of LQDE yield changes being driven by the benchmark government bond and 41% for IHYU.

Implied volatility of credit UCITS ETF Options cheap, US rates ETF IDTL in rich territory. IHYG and IHYU Options IVOL at a discount to realized

Implied volatility of 3-Month at-the-money Put Options was cheap versus the historical averages for all the credit underlyings. IHYG, which had implied volatility trading at 3.74 on July 27th, was more than one standard deviation cheaper than the historical average. Options on IDTL, which holds 20yr+ US Treasuries, were most expensive, pricing in 35% volatility, which was 1.85 standard deviations above the historical average and almost three times the 90-day historical volatility of the ETF. IDTL options traded the richest on a duration-adjusted basis as well, followed by IHYU and IHYG. These high yield ETFs exhibited the lowest volatility premium, with implied volatility 15%+ below the historical.

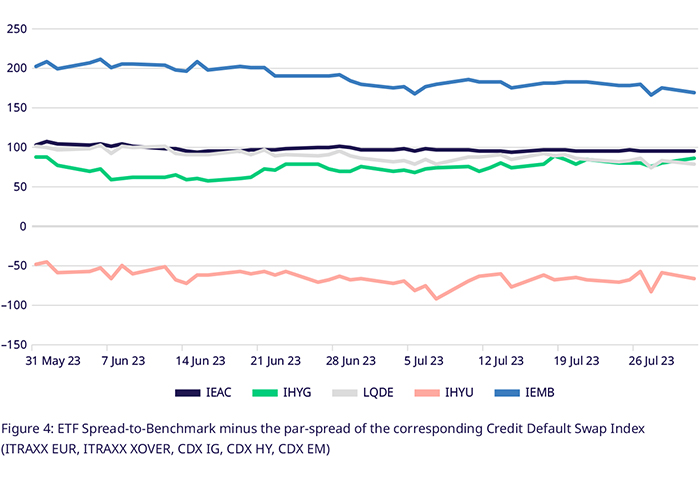

Basis between ETF Credit spreads and CDX spreads falls as ETFs prove more reactive to easing conditions than CDX

Credit Default Swap Indices (CDX) were less reactive to the bullish sentiment than the implied credit spreads of the ETF underlyings. The basis reduced 28bps for IHYG in early June but reverted to end the period almost flat. Similarly, the basis of IHYU, the only one out of the observed in negative territory, fell 44bps between May 31st and July, only to rise again, ending July with a basis 18bps lower than at the end of May. IEMB lost the most basis at 33bps over the period but has the highest basis in total against the 20-name Markit CDX Emerging Markets Index.

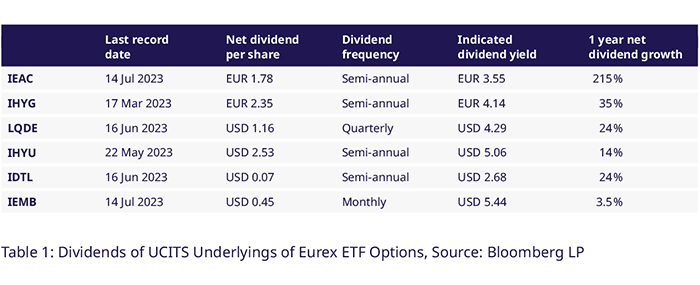

IDTL, LQDE, IEMB paid dividends in June. IEAC paid +215% YoY dividend in July

In June, IHYU paid an annualized gross dividend of $5.06 per share, +14.4%, since the last payment in late 2022. IEMB paid a $0.30 dividend per share, up 1.5% versus last year, while IDTL paid a $0.07 dividend per share, up 23.7% versus last year, combining a notional dividend yield of 2.7%. LQDE paid a $1.16 quarterly dividend per share, up 24% versus last year. IEAC saw its semi-annual dividend shoot up to €1.78 on massive inflows under higher yields.

Utilizing Eurex's Credit Futures & Options for Market Positioning

Eurex Credit Futures and Options enable you to hedge existing portfolios against duration and credit risk in one go. Eurex Options on Fixed Income ETFs allow for directional positioning while limiting options premium paid with options spreads or more tailored option strategies.

Thinking about trading US Interest rates and volatility using UCITS-compliant instruments? Gain exposure to US Treasury markets using the new Options on the IDBT (1-3yr Tenor) and IDTM (7-10yr Tenor) UCITS ETFs, launching on 4 September.

With our Bloomberg MSCI Euro Corporate SRI Index Futures (LXYA index) and Bloomberg Liquidity Screened Euro High Yield Bond Index Futures (AHWA Index), market neutral credit spread trades between EUR IG and HY are now also possible at Eurex.

Contacts