Mar 20, 2026

Eurex Clearing

Prisma Risk Management: Introduction for Bonds and Repos

1. Introduction

With this circular, Eurex Clearing announces the introduction of the portfolio-based Risk Management methodology (Prisma) for in-scope Bonds and Repos (Prisma Bonds) as well as enhancements to its current Risk Based Margining methodology (RBM) for the fixed income securities not migrating to Prisma yet.

As of 18 May 2026, on a mandatory basis, all Margin Parameters for Bonds and Repos as well as Fixed Income Securities Collateral haircuts (i.e. Eurex Clearing’s margin and default fund collateral haircuts) will be subject to an improved margin methodology (enhanced RBM).

Furthermore, Clearing Members can opt in via an activation form to benefit from Prisma bond portfolio margining (BPM). The activation will start as of 1 June 2026. Eurex Clearing will assign individual activation slots to Clearing Members based on the chronological order in which opt-in requests are received.

Member timeline:

By migrating the bond margin methodology to Prisma, a further harmonization of the margin methodology in the entire Eurex cleared fixed income securities and derivatives space is achieved. This will further deliver improved bond and repo portfolio-based margin offsets to Clearing Members and their clients and set the basis for further integration steps.

This initiative is expected to reduce the cost to centrally clear bond and repo transactions substantially and allows clients to manage euro interest rate risks more efficiently. Members should consider changes to Eurex Clearing’s risk reports if opting in for bond portfolio margining for Prisma Bonds.

In addition, there will be an improved calibration of margin parameters for FI securities not migrating to Prisma under the established RBM methodology (enhanced RBM), an improvement of the margin and default fund collateral valuation process, as well as an advanced modelling of bonds within the default fund calibration.

The migration of Bonds and Repos to Prisma is planned with the following approach:

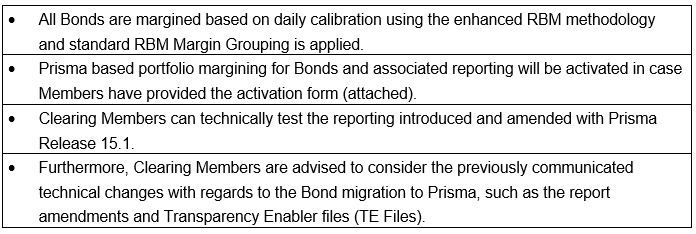

Simulation start (20 April 2026)

General:

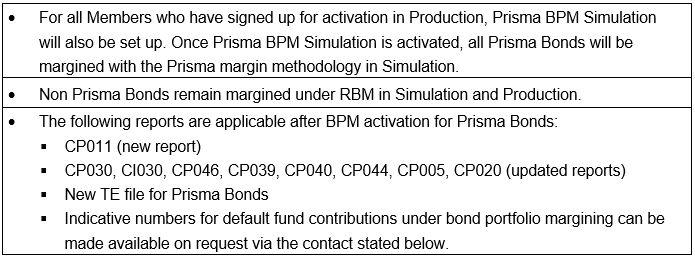

BPM activation:

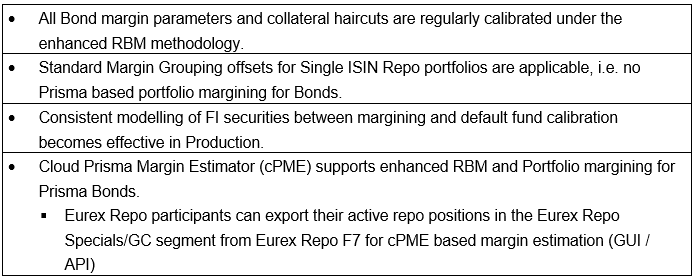

Production start enhanced RBM (18 May 2026):

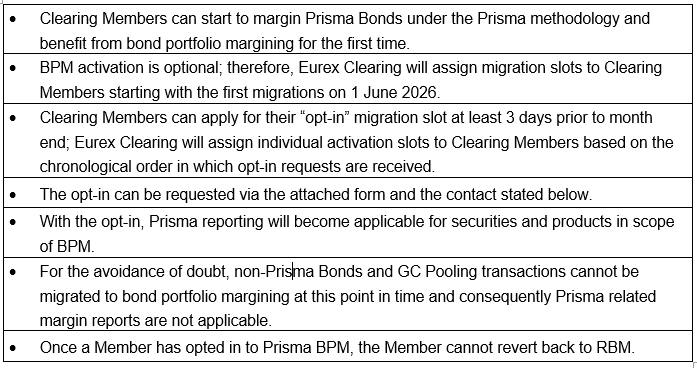

Production start BPM activation (1 June 2026):

Prisma Bonds:

The following Bonds denominated in euro are in scope for the switch to the Prisma methodology (Prisma Bonds):

2. Required action

Prisma and RBM will be offered in parallel for Bonds and Repos, allowing Clearing Members a smooth migration to the new risk method at their own pace via the opt-in offering. The migration of Bonds and Repos to Prisma requires Clearing Members and Vendors to consider/implement the following changes:

- Existing margin reports that cover products under Prisma will be changed and new reports have been introduced and announced with Prisma Releases 14.1, 15.0 and 15.1.

- An additional TE file containing information only for the Bonds and Repos in scope of the migration will be introduced with the changes in Simulation on 20 April 2026. Current TE Files will not change.

- If applicable, Clearing Members and Vendors need to adjust their reconciliation processes accordingly.

Furthermore, Clearing Members who want to benefit from Bond and Repo portfolio margining will be able to request the switch to Prisma for their portfolio of Bonds and Repos. The migration can be requested via attached activation form and the contacts listed below.

Updated documentation including a Report Reference Manual with details about the envisaged report changes and the new TE file have been made available in the Member Section of Deutsche Börse Group as part of the changes announced for December 2025.

3. Additional considerations

A. New TE File for Bonds and Repos

Certain fields in the new TE file “Bond Theoretical Prices and Instrument Config” relate to proprietary pricing processes and are provided solely as supplementary information. These fields, for example, comprise “Bond Type”, “Coupon Frequency”, or “Principal Redemption Pay Date”. They are not relevant to the risk model and may be disregarded unless the information is considered of interest. Please note that these fields may be removed in future versions, which will be communicated separately.

B. Introduction of new Supplementary Margin

With Production start on 18 May 2026, a new Supplementary Margin (SUBPM) will be introduced, measuring the difference between productive RBM-based margin of Prisma Bonds and simulated margin after opt-in. This will ensure that concentration risk of Prisma-eligible Bonds that are still margined via the RBM model is properly addressed. The new Supplementary Margin will therefore not apply after opt-in to portfolio margining.

C. Benefits

Introduction of Prisma methodology for Bonds will generate a number of tangible benefits to Cash Bond, Repo and Derivatives Clearing participants, i.e.

- Standardization of risk methodology across Bonds, over the counter (OTC) interest rate swaps and exchange traded derivatives clearing

- Improved reflection of Bond portfolio offsets

- Daily recalibration of Bond risk factors.

Following the implementation, Eurex Clearing will have delivered a key pillar for the future development of margin netting/cross product margining between Bonds/Repos and Derivatives.

For more information on Eurex Clearing’s Prisma model, please refer to the Eurex Clearing website www.eurex.com/ec/en/ under the following link: Eurex Clearing Prisma.

Unless the context requires otherwise, terms used and not otherwise defined in this circular shall have the meaning ascribed to them in the Clearing Conditions or FCM Clearing Conditions of Eurex Clearing AG, as applicable.

Attachment:

- Bond Portfolio Margining Activation Form

Further information

Recipients: | All Clearing Members, ISA Direct Clearing Members, Disclosed Direct Clients of Eurex Clearing AG and vendors | |

Target groups: | Front Office/Trading, Middle + Backoffice, IT/System Administration, Auditing/Security Coordination | |

Related circulars: | ||

| Contact: | client.services@eurex.com | |

| Web: | Prisma Release 15.1, Prisma Release 15.0, Prisma Release 14.1, Eurex Clearing Prisma | |

| Authorized by: | Manfred Matusza |