Aug 06, 2014

Eurex Clearing

Cross margining at Eurex Clearing, part 1

For many years the OTC market has been generally outside of the clearing realm, relying on bilateral collateral agreements to mitigate credit risk. Exchange products on the other hand, have been subject to clearing for a very long time. New regulations being applied to OTC markets are re-shaping the bilateral relationships into something much closer to the exchange world, and Eurex Clearing is now positioned to combine both markets to bring reductions in margin costs and a cross-market risk management approach.

What is Prisma?

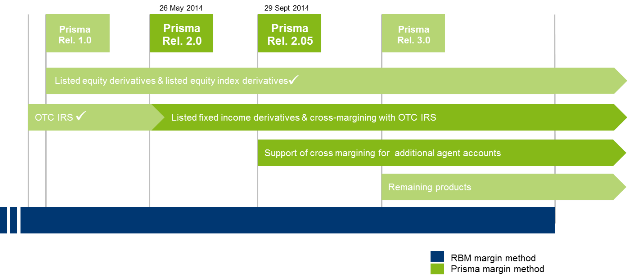

Eurex Clearing Prisma, short for Portfolio Risk Management, is the new method which calculates risk across underlying products and even across multiple markets cleared by Eurex Clearing. The clearing house is moving all its cleared products to Prisma over time, starting in 2013 with all equity and equity index products and, with release 2 in May 2014, moved all fixed income products to this advanced risk method.

The latest release not only offers the ability to benefit from portfolio margining within an asset class but also to additionally offset the OTC and ETD markets. Alongside the development of Prisma is the fundamental concept of liquidation groups, providing a framework for managing risk of similar products in a common way and offering full margin offsetting within these product groups.

What is a Liquidation Group?

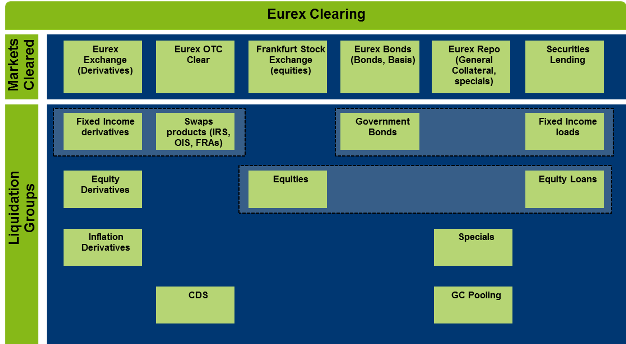

A Clearing Member’s portfolio typically features a diverse structure, size and/or complexity. Given that complexity, and due to the general handling principles laid out in the default management process, it is usually impossible to liquidate an entire portfolio in one single transaction. Therefore, Prisma introduced the concept of liquidation groups.

A liquidation group combines cleared products across markets cleared by Eurex Clearing that share similar risk profiles. Liquidation groups serve as a cornerstone of the Prisma portfolio-based risk management method and offer full margin offsetting capabilities per group.

• Liquidation groups are pre-defined; they exist irrespective of a clearing member default.

• Setup of liquidation groups, i.e. what products go into the available groups, is a matter of

liquidation process style, risk factor proximity, hedging and pricing ability.

• Portfolio risk margin offsets are only granted within these pre-defined liquidation groups.

• Each liquidation group has a fixed holding period that reflects the time estimated to analyze,

hedge and auction the respective products. An expected holding period can be between two

to five days, depending on the liquidation group, and is the basis for margin calculation at

the same time. Equities, for example, are calculated with a four-day holding period (i.e.

four-day P&Ls), listed fixed income are calculated with two and OTC products – for

regulatory reasons – with five days.

What are the benefits?

There are multiple benefits attached to the general setup – both for clearing members and the clearing house alike.

Clearing members obviously benefit from the fact that with Prisma margins are not calculated on a granular product underlying level anymore but rather on a liquidation group-wide portfolio approach. This alone caters for margin reductions of up to 70% depending on the individual participant’s portfolio structure. For instance, well-balanced, non-directional positions benefit more due to larger offsetting positions.

With Prisma release 2, and the introduction of listed fixed income products, a whole new level of margin savings is achieved, as members now are able to hold their ETD exposure together with their OTC risk in one single liquidation group. If a member default were to occur, the clearing house would treat this liquidation group as a joint portfolio and hedge and auction it off together. This is the main reason Eurex Clearing can factor in the margin offsetting right from the millisecond members clear a position, be it ETD or OTC.

Just by activating the cross margin optimiser, Buy Side and Sell Side alike get to potentially save up to 60-70% margin cost due to the fact that, for instance, a Bund future serves as a natural hedge against a 10y interest rate swap in the fixed income liquidation group.

(First published by The OTC Space)