Jul 18, 2014

Eurex Clearing

Cross margining benefits from Eurex Clearing

With Eurex Clearing Prisma Release 2.0 on 26 May 2014, we are now offering cross margining between Eurex fixed income futures products and interest rate swaps (IRS). This generates significant margin and collateral savings for both the sell- and buyside for fixed income portfolios of EUR IRS and EUR listed derivative products.

The cross margining of a portfolio of EUR IRS and fixed income futures and options products, as the example below shows, gives both the buyside and sellside significant margin savings.

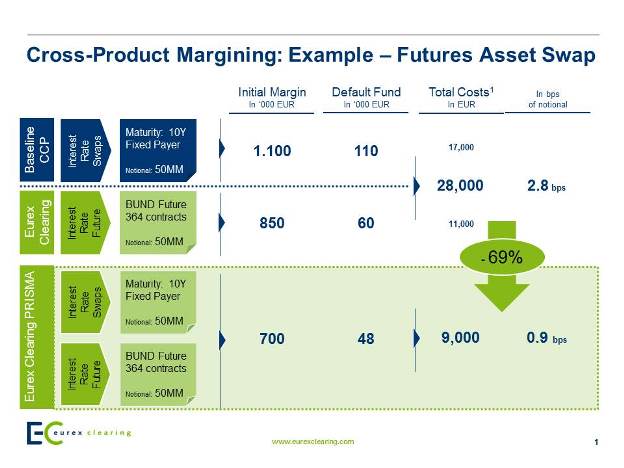

A ten year Euro asset swap trade is a good example to show the benefits of clearing EUR interest rate swaps and listed derivatives products at Eurex Clearing.

A margin and capital cost comparison (see graph below) was made of initiating a EUR 50 million asset swap consisting of a Bund Future/Ten Year Euro IRS across a baseline CCP for the EUR IRS and Eurex Clearing for the Bund Future compared to clearing both IRS and Future of the Asset Swap through Eurex Clearing.

The result: The lower margin requirement through cross margining and the lower default fund contribution reduces the cost to the sell side of the asset swap transaction by 69 percent.

We would be happy to speak more about our cross margining capabilities with you.

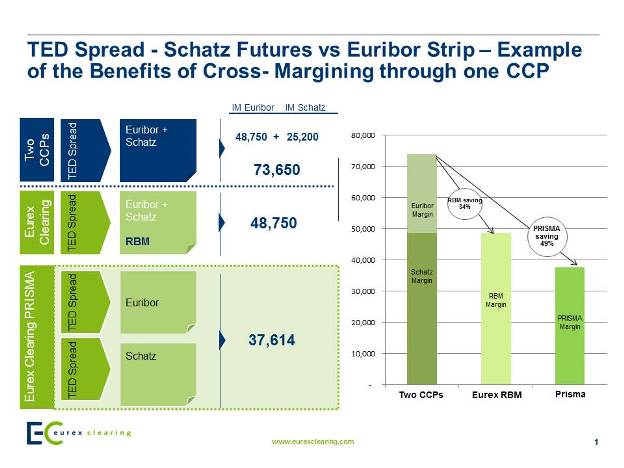

The benefits of cross margining can be seen by the margin savings of a relative value DV01 neutral trade between a EURIBOR Strip and Schatz Futures ('Term Ted'). Margin savings are 49 percent with Eurex Clearing Prisma compared to clearing through two different CCPs. In addition, the sell side benefits of the lower capital regulatory requirement through the netting of exposures.

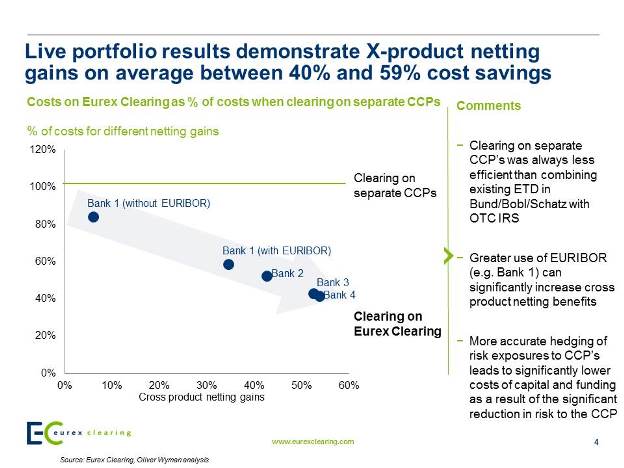

In the graph below you can see actual results from a sellside cross margining case study. We compared four actual sellside bank portfolios of EUR listed derivatives and EUR interest rate swaps (IRS) cleared through Eurex Clearing compared to several other CCPs. The result shows that using Eurex Clearing generates margin efficiencies of 40% - 50%, not to mention the lower capital regulatory requirements through clearing listed derivatives and IRS through a single integrated CCP.

We would be happy to speak more about our cross margining capabilities with you.

Eurex Clearing AG

Clearing Business Relations