Apr 08, 2022

Eurex

Equity Index market briefing April 2022

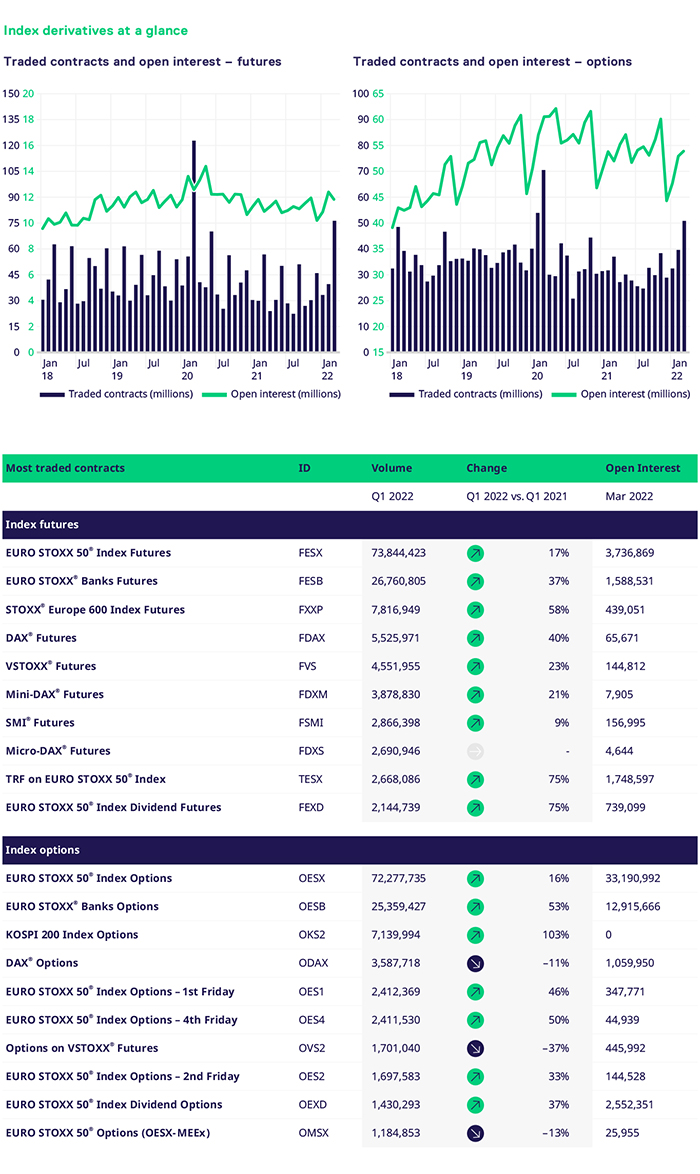

This quarter will be remembered for all the wrong reasons, unfortunately. The subsequent spike in volatility for financial and commodity markets has reverberated into the real economy. Governments find themselves walking a tightrope of fiscal and monetary policy responsibility. The unstable macroeconomic and political picture has led to an immediate increase in demand to hedge and efficiently reposition portfolios. This naturally drives the high trading activity in futures and options at Eurex. Realized and implied volatility levels have remained above long-term averages after the initial shock from the Ukraine invasion. The March-June roll provided further impetus to this particularly pronounced volume uplift. Overall, we saw monthly records in March for Sector derivatives, the Micro-futures segment, Mini-DAX®, MSCI index derivatives and TRFs. New quarterly volume records were reached for our ESG and FTSE index derivative product suites.

Despite the challenging market conditions, members remained highly supportive of several new product launch initiatives. A range of new EUR denominated Equity TRFs were added to enhance the appeal of the related Basket TRFs. We expanded the MSCI segment with the listing of China and Saudi Arabia index options, as well as index futures on Germany and Israel. We also added new ESG screened index derivatives on MSCI Europe and MSCI EMU. The most recent introduction on the index side was the successful launch of the KOSPI weekly index options, where good early volumes were printed. We also listed various new single stock derivatives that met our listing criteria, including several SEK denominated dividend futures.

Current plans for Q2 will see several exciting new product launches, details to be published shortly. Although the reverberations of the Russian sanctions have already been felt, this storyline is far from over, with potential new sanctions on the horizon, touching the European oil and gas markets. That is unless a diplomatic solution and de-escalation of war can be achieved, which we all hope for. Another event risk for European markets is unfolding with the French presidential elections later this month. This leads me to anticipate that elevated volatility will persist in the coming weeks and months.