Jan 10, 2022

Eurex

Equity Index market briefing January 2022

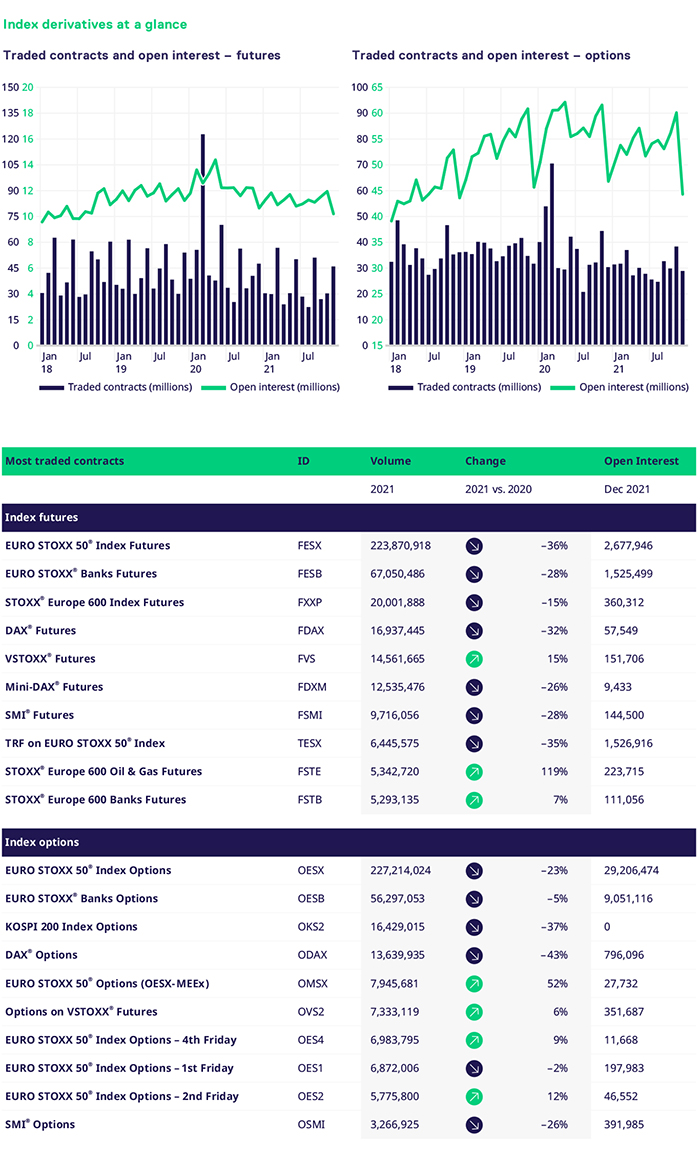

Looking back at the tremendous equity market returns, one could easily conclude that 2021 was a steady and typical bull market. However, nothing would be further from the truth. IPO markets remained hot in Europe with a similar picture in the U.S., where the SPAC activity remained buoyant. The crypto market capitalization set new records amid high trading volatility. Violent short squeezes in meme stocks pushed the balance of power away from hedge funds into the hands of the retail herd. The macro-economic picture also shifted from the initially positive but bumpy recovery from the pandemic to real fears of surging global inflation. Unfortunately, some dismal records were also set in terms of extreme weather conditions and further evidence of highly damaging global warming.

For Eurex, it was an active year for new product launches, commencing with broadening our successful TRF segment by adding the FTSE 100 index. Further expansion of our ESG offering across MSCI and STOXX® index solutions enabled investors to react to the fast-moving sustainability regulation changes. Eurex also listed a suite of micro futures based on our key benchmarks to address the visible increase in retail participation. Staying on the theme of popular asset classes amongst retail is of course crypto and our Bitcoin ETN futures brought successfully to market, aimed at opening the doors further to institutional investors. Given 2021 represented a recovery phase from the turmoil of the preceding year, there were still some notable volume growth stories. Our leading global position in MSCI derivatives was further enhanced; the same was observed for our ESG index segment. Among the more established products, the stand-outs were VSTOXX®, STOXX® Europe 600 and sector derivatives.