May 05, 2022

Eurex

Equity Index market briefing May 2022

In April, there seemed nowhere to hide with investors experiencing challenges adapting to the new interest rate regime. We now enter a distinctly hawkish period from a double-decade era of lower and lower interest rates that fueled price appreciation across all asset classes. For many market participants, higher yields were unseen and the impact on equity markets has been swift and severe. Valuations are being reassessed, and a bear market sentiment prevails. For example, there is a gathering chorus of dissenters critiquing cryptocurrencies again. Rather, I have always considered this a healthy development as you need different opinions to create a truly two-way market. As measured by our VSTOXX® futures, implied volatility has remained stubbornly above 30%, reflecting the dramatic shift in market dynamics.

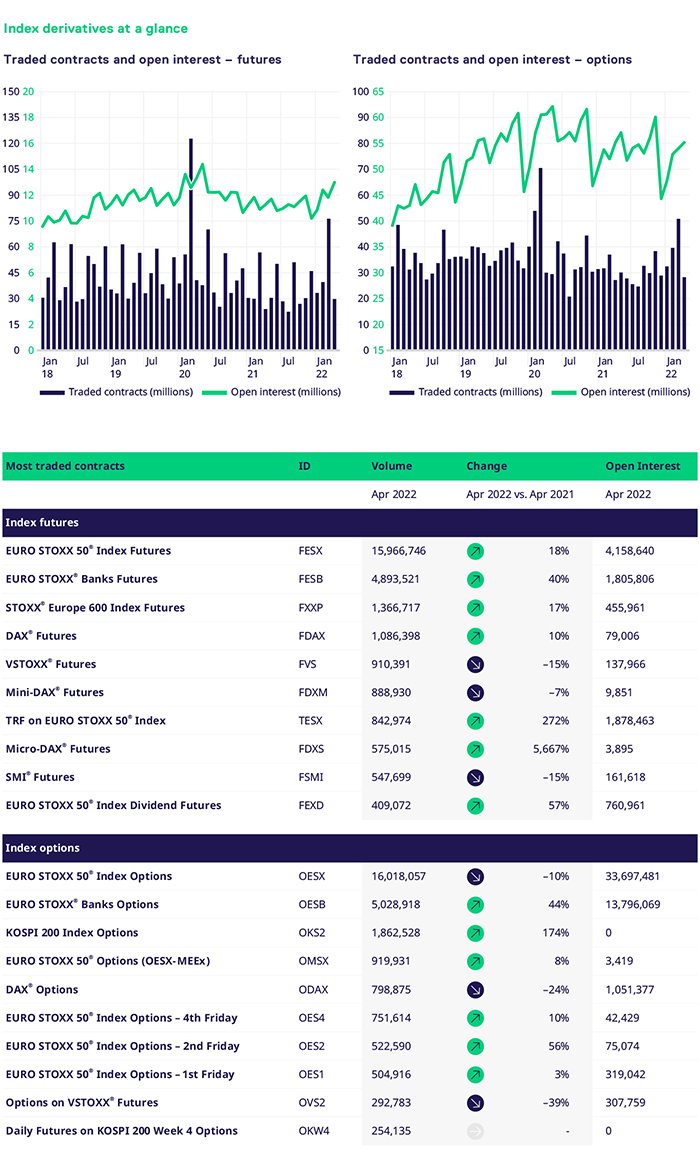

Understandably, the highest volumes once again have been in our benchmark products, EURO STOXX 50®, Banks sector, STOXX® Europe 600, DAX® & Micro-DAX®, TRF and EURO STOXX 50® dividend futures. The recently launched KOSPI index weekly options already represent ~40% of total KOPSI options volumes at Eurex. Naturally, with the increased uncertainty, hedging demand has been the driver of on-exchange activity. Moving from “buy-the-dip” to a “sell-the-bounce” regime is a tough pivot for any trader to make quickly. However, Eurex’s highly liquid futures and options products can facilitate such tactical changes efficiently.

We aim to focus our attention on delivering value to members and clients across the product portfolio by extending our offering in the Banks® sector dividend derivatives. Here, listed solutions continue to draw strong investor interest. We also anticipate renewed interest in our EURO STOXX 50® Quanto USD futures, given the sharp divergence in interest rates between the U.S. and the Eurozone, impacting currency movements. There will be further targeted product launches in what remains of Q2, particularly on the index futures side, where we predict a good level of long-term demand.