Sep 06, 2022

Eurex

Equity Index market briefing September 2022

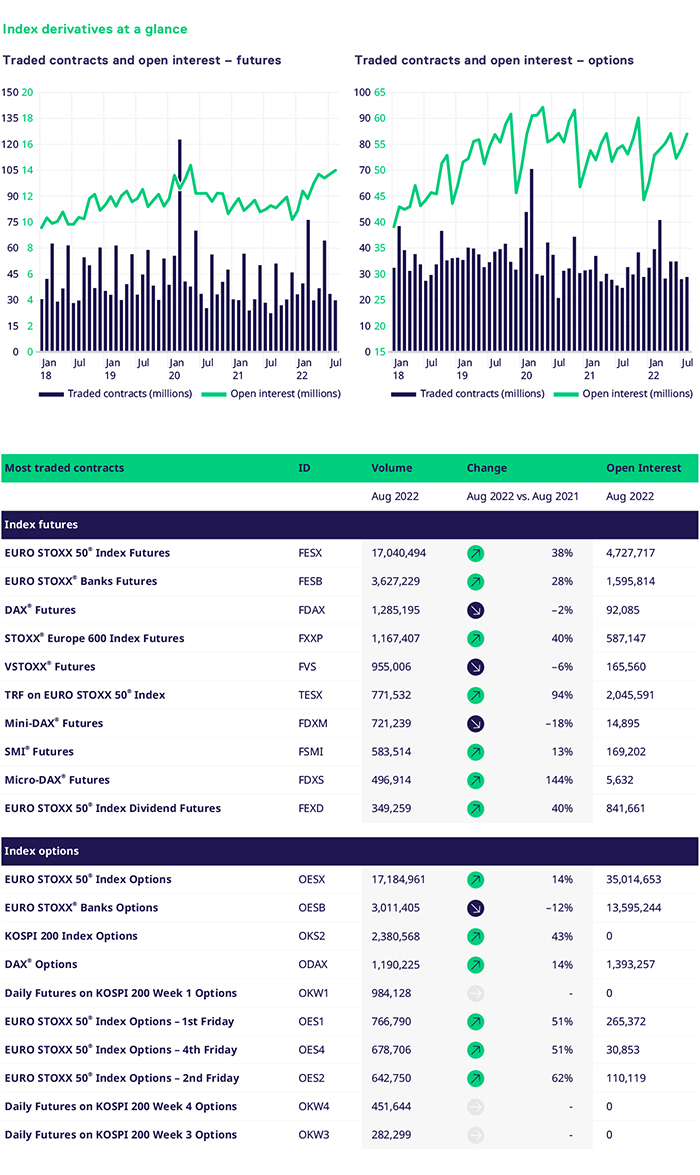

Strong volumes across Eurex’s equity index benchmark products

For those who managed to take a well-earned holiday in August, you probably still spent some of that relaxation time discussing or contemplating the many challenges we face today. No amount of sun, sand and sea can deflect the real-world state; the protracted war in Ukraine, droughts in several parts of the globe, devasting floods in others, burning forests in the heatwave and sharply rising energy costs. The markets mirrored this gloomy outlook, with both bond and equity benchmarks performing negatively as an attempted mid-month rally rapidly faltered.

Given this backdrop, derivatives usage remained robust and saw strong volumes across Eurex’s index benchmarks. The volume growth was most interesting in our FTSE segment, where market participants increasingly embrace the FTSE 100 TRF to achieve U.K. equity market exposure without the need to reference the increasingly volatile GBP short-term interest rate futures strip market that impacts forward pricing. Despite the recent media debate around the relative merits of ESG investing, we saw new trading activity in our EURO STOXX 50® and DAX ESG weekly index options that demonstrate interest is still present. Open interest levels in our MSCI derivatives segment approached highs again with good activity in EM Asia, World, ACWI futures and EM options compared to the same month last year. Sector index futures were also relatively active, with the highest volumes in Banks, Oil & Gas, Autos and Telcos.

With the late Q3 and early Q4 periods being statistically weak for equity markets, central banks will be put under immense political pressure to either justify their determination to stay on a tightening policy path and defeat inflation or bow to the negative consumer wealth impacts and soften this stance accordingly. Regardless of the future route, we can expect that Eurex’s deep and liquid derivatives markets will be needed to facilitate further hedging demand.