Jul 25, 2016

Eurex

Eurex Exchange's Equity Index Derivatives news - Q2/2016

The trading volumes in Q2/2016 show very robust interest in Equity Index Derivatives. The quarter started quietly with volatility as measured by VSTOXX® at comparatively low levels (under 25 index points). However, due to the uncertainty relating to the U.K. referendum, the market volatility and trading volumes spiked dramatically in June. In fact, June 2016 was the strongest month in terms of volumes in five years. Over 245 million futures and options contracts were traded in the first half of this year.

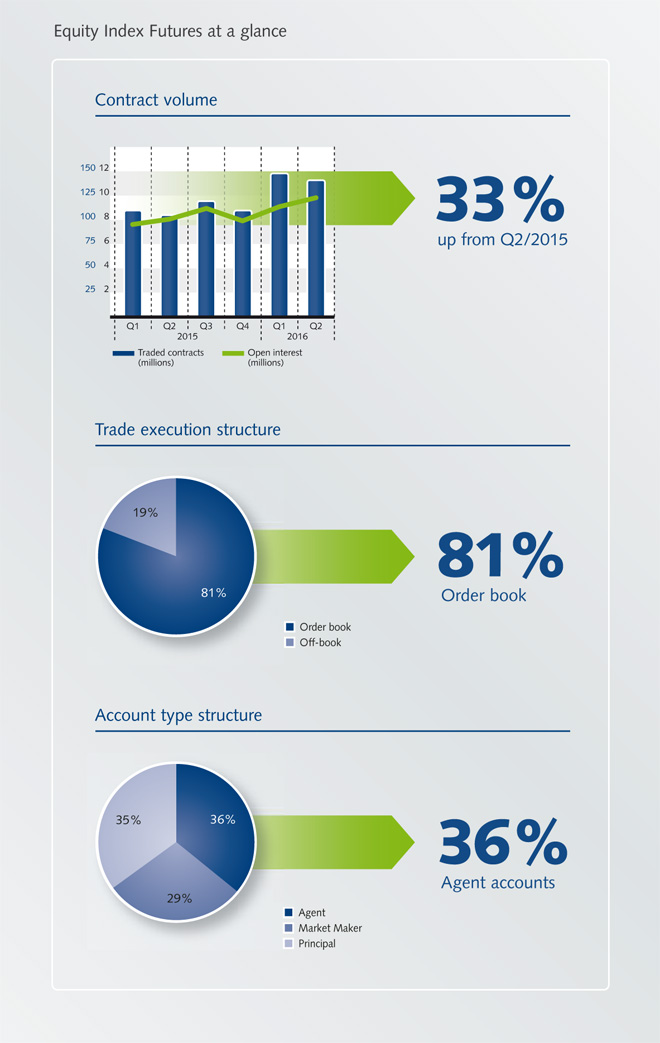

Futures at a glance

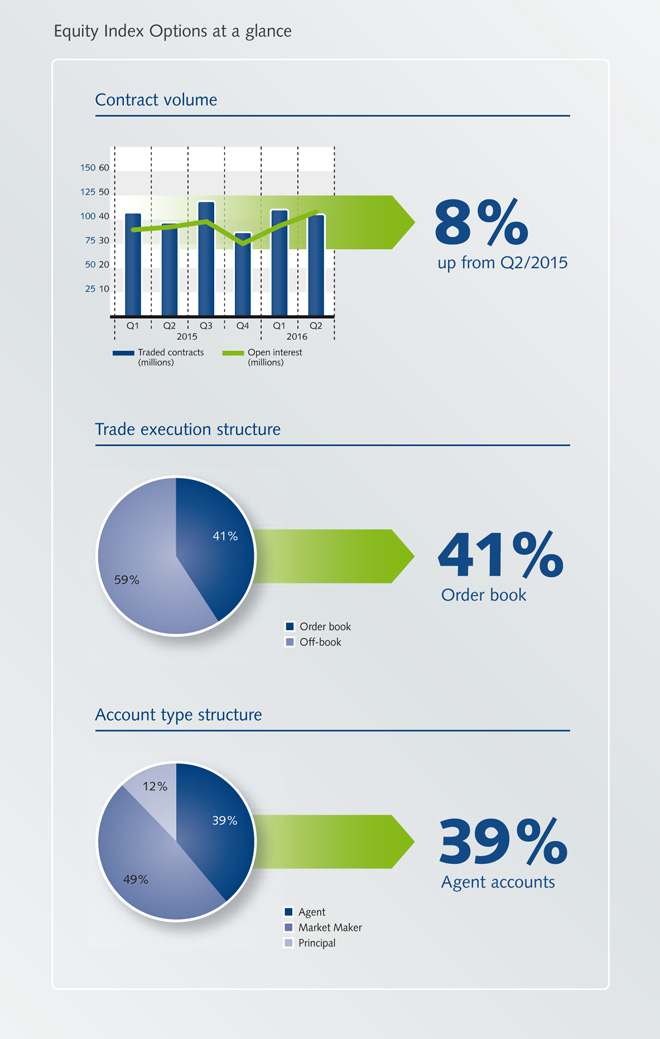

Options at a glance

The increased market volatility in the last quarter took a toll on options volume. Breaking this trend were options on financials, such as, EURO STOXX® Banks Options and STOXX® Europe 600 Bank Options which increased by 101% and 104%, respectively. SMI® Options were also a strong performer, showing a rise of 29%.

Top performers

Futures volume increased markedly across the whole spectrum of index futures when compared to the same period in 2015. The MSCI Europe Futures have shown the most spectacular increase in trading volume, a 932% rise. The STOXX® Europe 600 was also very actively traded, showing a 123% increase in volume. This benchmark is popular with investors who increasingly prefer pan-European exposure over single country allocation. Bank headlines and the subsequent price turbulence translated into strong interest in trading financials. As a result, the volume in EURO STOXX® Banks Futures and STOXX® Europe 600 Banks Futures rose by 73% and 60% respectively.

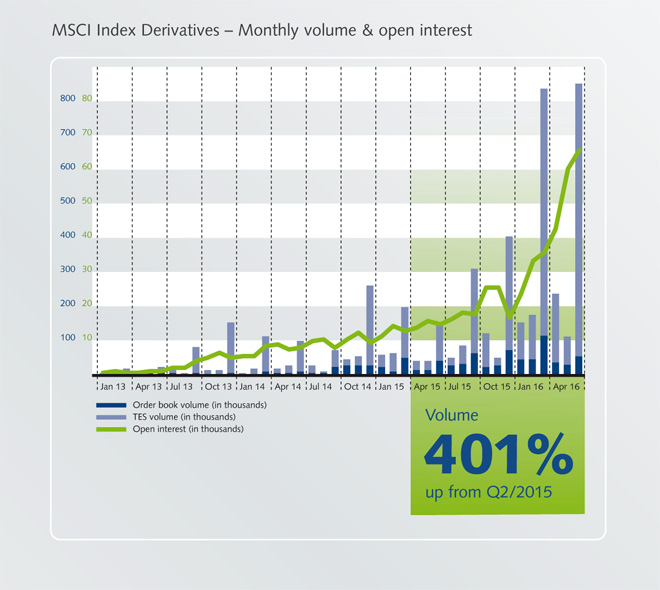

MSCI Derivatives

More than 1.2 million contracts were traded in Q2/2016, in comparison to 239,378 in Q2/2015. This represents over a fivefold increase. Eurex saw over 700,000 MSCI Futures and Options traded in June with MSCI Europe, World and EM Asia futures trading 382,000, 164,000 and 119,000 contracts respectively. This is the most active month to date. Over 2.2 million contracts have traded so far in 2016, this compares to 1.6 million for the entire 2015.

VSTOXX® Derivatives

The European benchmark for volatility keeps on growing. June 2016 was the best month ever for the volatility product suite, particularly for the VSTOXX® Futures, with a record daily volume at 110,000 and a monthly record of 1.2 million contracts. At all times during periods of heightened volatility caused by Brexit, the futures were 0.05 to 0.1 points wide, providing trading and hedging opportunities for the market participants.