Jan 14, 2020

Eurex | Eurex Clearing | Eurex Group

Euro clearing in Frankfurt: Excellent developments in 2019 and a positive outlook into 2020

It’s been a while since I updated you on euro clearing in Frankfurt, so I thought the new year would be a good time to do so and to share my optimism regarding growing volumes and our continued competitiveness.

And this optimism is related to the increasing activity we continue to see on the buy side.

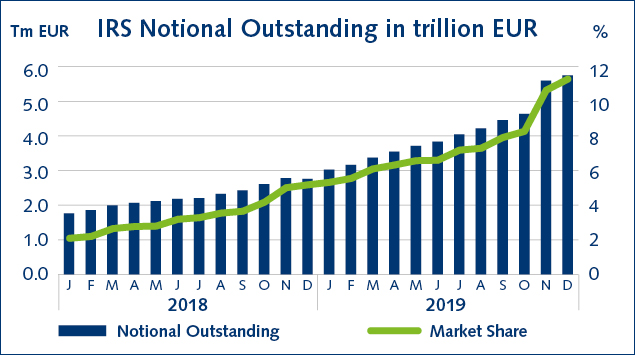

Our total notional outstanding of almost EUR 13 trillion, as of 31 December 2019, keeps our overall market share at nearly 15 percent. The market share in IRS notional outstanding has increased to over 11 percent end of December – up from around 6 percent twelve months ago.

This is a sign of increasing buy-side activity as these market participants tend towards opening longer dated directional positions. This development is also confirmed by a strong growth in OTC IRD Initial Margin, which has more than doubled in the last 12 months to now almost EUR 12 billion.

Client numbers are also extremely encouraging:

We currently have over 300 clients onboarded, up by 170 who on-boarded in 2019, and the number of regularly active clients goes hand-in-hand with these developments. As you may have seen reported in November, Dekabank switched a substantial portion of their swap book from LCH to Eurex. Switching 7,000 trades in just a few hours clearly demonstrates that these types of moves are technically feasible and, obviously, economically viable.

So our alternative EU-based liquidity pool for Euro Swaps continues to grow. I am therefore optimistic that – whatever political developments we see in the coming months – we will continue to competitively facilitate euro clearing in Frankfurt. Indeed, in December we cleared our first €STR overnight index swaps at Eurex, with participation from several major banks.

I wish you all a happy and productive start to 2020, and I look forward to catching up with many of you at our Derivatives Forum on 27 February in Frankfurt.