Oct 30, 2018

Eurex | Eurex Clearing

Euro swap clearing in the EU27 – a macro view on buy-side execution costs

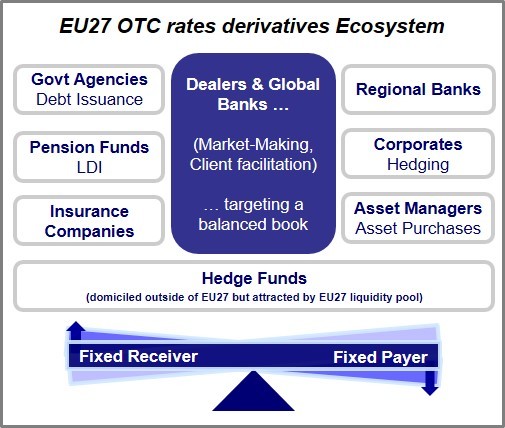

The market for rates in the EU27 is perfectly diversified and home to a wide spectrum of market participants. To achieve a balance in its client flow (pay vs receive fixed) is one key success factor for central-counterparties. Since Eurex Clearing is well advanced in achieving this goal, dealer banks are able to balance their books within the Eurex Clearing ecosystem and buy-side execution prices at Eurex Clearing are competitive.

The EU27 rates market – a healthy and well diversified ecosystem

The EU27 is, much like the global rates markets, home to many-faceted rates views and interests. Dealer banks that mainly serve as intermediaries between the client’s interest to pay or receive fixed rates are matching the demand. Global arbitrageurs are adding to the ecosystem but are capitalizing on other trading strategies.

A diversified CCP client base enables competitive execution costs – the key to success

Clearing costs are mostly driven by non-transaction costs, e.g. clearing broker and CCP fees, margin funding and transaction costs for execution like bid-offer spreads and CCP-basis driven price differentials. Execution costs charged by dealer banks need to cover the brokers clearing related capital costs, business operating costs, own CCP fees, and market-making profit-margins incl. any risk premiums. This makes buy-side execution costs sensitive to changes in the supply and demand balance at a specific CCP as market making dealers are targeting a balanced book (excl. other factors affecting their books). Hence, CCP specific bid-offer spreads and price differentials may serve as a balance indicator of a CCP’s client base and the healthiness and liquidity of its OTC rates ecosystem.

Market observed execution costs for Eurex Clearing indicate a healthy rates ecosystem

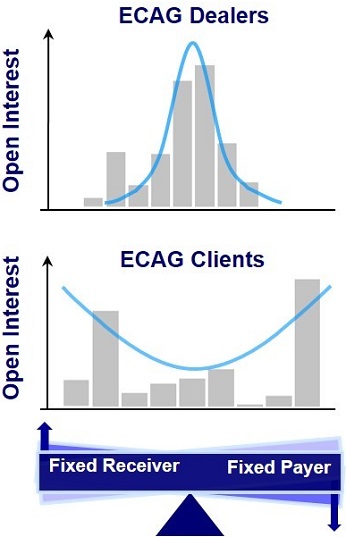

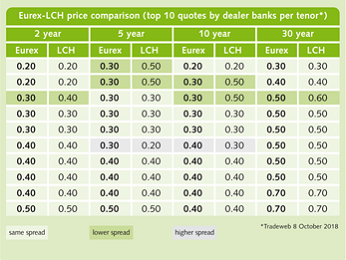

Member activity and clearing volumes at Eurex Clearing have significantly increased in 2018. The market makers quote prices for pay and receive fixed rates at bid-offer spreads comparable to LCH. Thus, the EUR IRS price differentials across all maturities for Eurex Clearing and LCH have converged.

Market makers benefit through balancing their books within the Eurex Clearing ecosystem for a wide range of maturities. In addition, Eurex Clearing’s ecosystem encompasses increasingly balanced client supply and demand.

All that makes running a split outright EUR book and hedging across CCPs increasingly unnecessary.

Eurex Clearing buy-side execution costs converge to competitive levels

Given the balanced CCP client supply and demand there is no rational argument for a significant CCP basis or erratic move thereof.