Dec 02, 2020

Eurex

Fixed Income market briefing December 2020

November has seen mixed volumes across the Fixed Income (FIC) portfolio. The futures suite saw a robust pick up in volumes +4.8%. Within the core German futures segment, Schatz and Buxl futures had a month-on-month growth of 21.1% and 55.7%, respectively. Buxl futures volumes continued to benefit from a combination of better realized in the underlying futures and flows from Buxl Options, which saw c.41.7k of contracts trade in the month. Total volumes in the newly launch Buxl options are c.78k (2k ADV). Overall, the options segment saw lower volumes across the board, except for the Schatz complex, which was +38.7% compared to last November. Underlying rates markets have remained in tight ranges, with bouts of volatility being short and tense. FIC volatility remains at historically low levels despite concerns of overheated equity and credit markets.

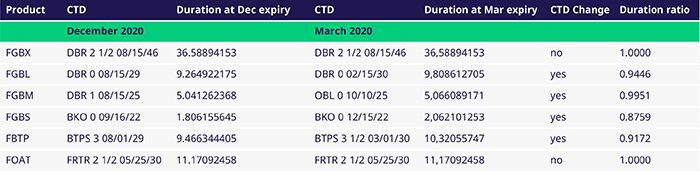

Overview of the futures CTD across expiries

The fixed income futures roll to the March 2021 contracts saw a change of the cheapest-to-deliver bond (CTD) in three out of four German benchmark futures. This change is relatively rare, as the CTD change in the Bund (10-year) futures usually happens only once or twice a year simultaneously with Bobl (5-year) futures. Also, the 10-year BTP futures changed CTD.

The duration of the new CTDs is greater than the previous CTD. Therefore, when rolling to the next expiry, the futures exposure needed to hedge the same amount of risk was lower. This was reflected in the duration ratios between the two bonds in the underlying deliverable basket; to get the same exposure of 1,000 December 2020 Bund contracts, you only needed 944 March 2021 contracts.

The increased duration of the new CTD for the three German futures was mirrored in the reduced number of re-opened positions in the March 2021 expiry (after futures delivery), reflecting the stronger hedging power of the new CTDs.

November was the strongest month for FIC ETF options, with c.96.5k contracts trading in total. This was across two underlying's, the U.S. High Yield Corporate Bond ETF and the U.S. +20y Treasury ETF. The volume in the U.S. Treasury ETF was the equivalent to c. $1bn of the underlying ETF. Support from our members in this segment has been strong and this is a segment which we see continuing its momentum across the Eurex franchise.

Looking ahead into year-end, there is enough for the market to digest due to event risk and rolls, which should support volumes. In closing, we would like to extend our gratitude to our members for supporting our initiatives throughout the year; it is much appreciated.

Lee Bartholomew, Head of Fixed Income Product R&D, Eurex