Jan 05, 2023

Eurex

Fixed Income market briefing January 2023

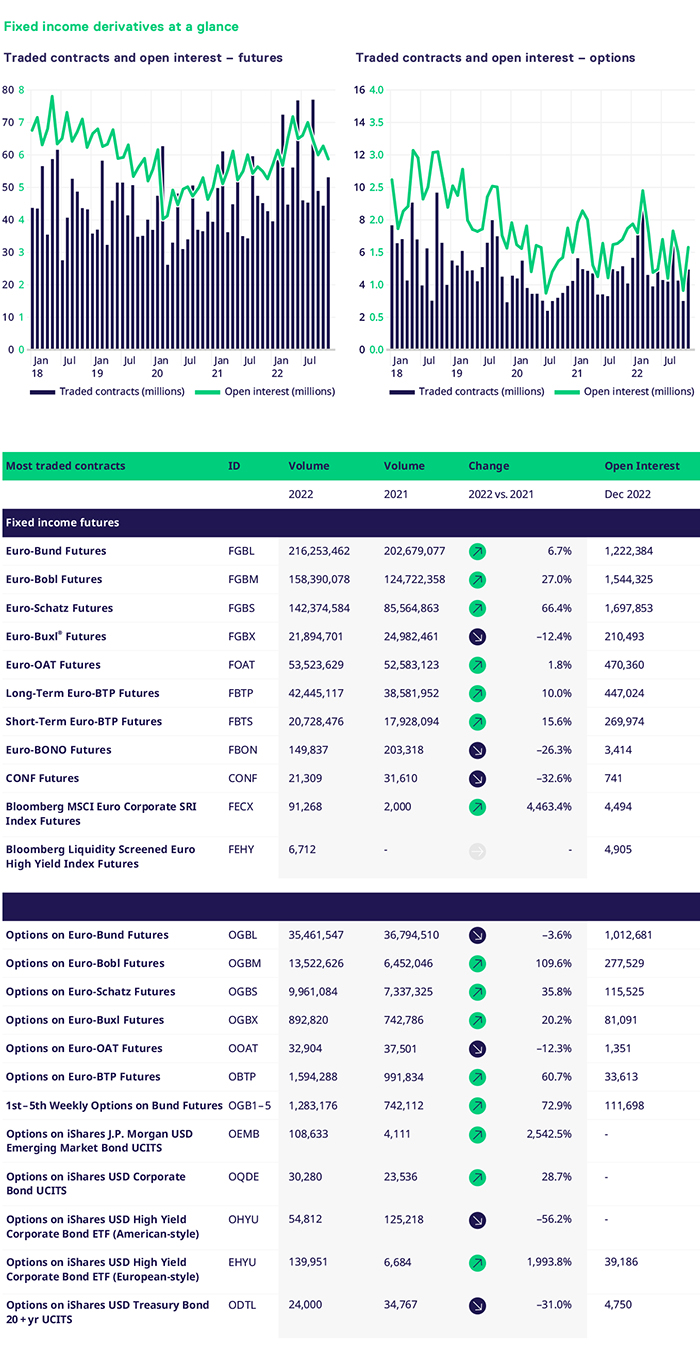

Growth in major Eurex fixed income products accompanied by a rotation to short duration in 2022

When we enter a new year, we can build on the previous year's learnings, momentum, challenges and insights. This can be the positive aspects as well as the elements that provided us with challenges. Like many businesses, we will face headwinds in 2023, yet we have much to look forward to. The team has a comprehensive roadmap of initiatives we will execute, working closely with our colleagues, clients, members and stakeholders. Looking back on 2022, the core portfolio performed solidly, with volumes seeing a c.21% year-on-year (YoY) increase versus 2021. This was an impressive achievement, given the performance of the Fixed Income business in the previous year.

Our members, clients, liquidity providers and colleagues from across the business worked closely with the team to bring our initiatives to market while ensuring that our core markets functioned smoothly in the volatile environment. Nascent segments, like credit, ETF options, ESG and FX were well supported, which enabled the volumes to evolve in line with expectations, increasing year on year.

2022 was characterized by higher intraday volatility which helped to underpin our core futures segment. We saw a rotation to short duration that saw the front end of the German and Italian curves outperform. Schatz futures volumes were 66.4% higher versus 2021 and Italian BTS futures saw an increase of 32% YoY . Bobl and Bund futures were 27% and 6.7% higher versus 2021, with the Italian and French 10y segments 10% and 1.8% above 2021 levels. The long end of the German curve was coming off a strong 2021, which meant volumes were 12.4% lower versus 2021.

Looking at December in isolation, the business performed strongly across the board. Futures saw an increase in volumes of 24.5%. All the core segments had double-digit growth except for the long end. Bunds, Bobl and Schatz were 19.6%, 19.8% and 60.4% higher, respectively. The front end of the Italian curve outperformed and ended 51.8% higher versus December 2021. The Italian 10y segment was 16.1% higher. ESG credit futures traded 13k for the month, a significant improvement compared to the prior year.

With intraday volatility high (we moved from single digits 4.6% to over 14% at times), options volumes were well supported. The Italian segment outperformed relative to the previous year, seeing an increase in volumes of 86% YoY. Bobl, Schatz and Buxl options were double digit higher versus the previous year, 127%, 40% and 31% , respectively. Bund options were a story of two halves. The core options saw a decline of 3.6% versus an increase of 72.9% for weekly expiries.

The options segment performed solidly, 31% higher versus the prior December. This time we had a reversal of performance, with Buxl options outperforming, trading 201k, 190% above December 2021. Bund and Bobl options traded 41% and 52% higher and Schatz underperformed by 54.5%.

Moving away from core rates, there is much to fill the team with optimism. The ESG corporate bond SRI futures traded c.91k contracts and saw open interest grow to c.4.5k contracts. At stages throughout the year, the contract was the second-largest ESG futures contract globally across all asset classes when measured by OI. This is an impressive achievement and gives the team confidence that we are building our portfolio to support structural themes. Another reason for the volume growth came from the team's tenacious approach to cultivating the segment with our clients, liquidity providers and members. The launch of our High Yield futures contract further underpins our commitment to this segment. It was a natural extension of the product portfolio and volumes have been developing nicely. We saw 6.7k contracts trade in December. We focus on building on 2022's momentum to further develop these two segments.

With credit spreads widening and volatility trickling into credit, our ETF segment performed strongly YoY. There were several bright spots, including Emerging Markets, Corporate Bonds and USD HY corporate bonds, all seeing solid pick up in volumes. The outperformers were the Emerging Markets and USD HY Corporate Bond underlyings, with volumes 2542% and 1993% higher versus 2021. Coupled with increased volatility, higher rates and wider spreads, the ETF options are well-positioned to grow further in 2023. Liquidity is solid, with clients able to execute c.$700m equivalent of the underlying ETF. As a result, the team continues to develop new insights and analytical tools to help clients better understand the segment from a risk and execution perspective.

The FX segment continued its strong momentum into the year's second half, with the team working closely with key sell and buy-side clients on readiness. Building critical mass is something that the team is focused on and we were able to accelerate this in the second half. The team and I are hopeful that we can continue to build out this important sector enabling clients more flexibility in their execution. For December, volumes in the FX portfolio were 67.4% higher as new clearing members went live. Looking at the performance over the year, volumes were up 130.9% versus 2021. The USD/KRW was the standout sector, with volumes 391% above 2021 levels.

Considering the above, the team and I are excited by the prospects of this coming year. We have a comprehensive roadmap of initiatives, with ESTR futures scheduled for 23 January. Building this segment is a natural extension of our product portfolio and we will work consciously with our members to establish it. Our approach is always to work with our members, clients and liquidity providers to build a comprehensive yet diverse ecosystem that supports their needs. For this reason, we are confident that we can deliver on our commitments.

I said throughout last year that our business is built on the depth of our relationships with our clients, members, liquidity providers and colleagues. Without their support, none of this would be possible. I was enormously impressed with the focus, commitment and execution in 2022. Personally, and sincerely, a huge thank you. I am humbled to work with such inspiring people.

Looking ahead to 2023, as a team, we feel the business is positioned to support the key structural trends in place across FIC. The expectation is that volatility will remain elevated, and underlying markets will continue to test new highs and see decent two-way price action. FX is likely to see increased focus, together with credit coming more into the spotlight. The new initiatives the team will bring to market will help to further strengthen our portfolio.