Oct 11, 2024

Eurex

Fixed Income market briefing November 2024

Record volumes in Credit Index Futures and FX in October

October 2024 continued the upward trend for the FIC portfolio, while geopolitical tensions, the US elections and expected actions of the Fed, ECB and BOE continued to play in the mind of market participants, boosting volatility and volumes.

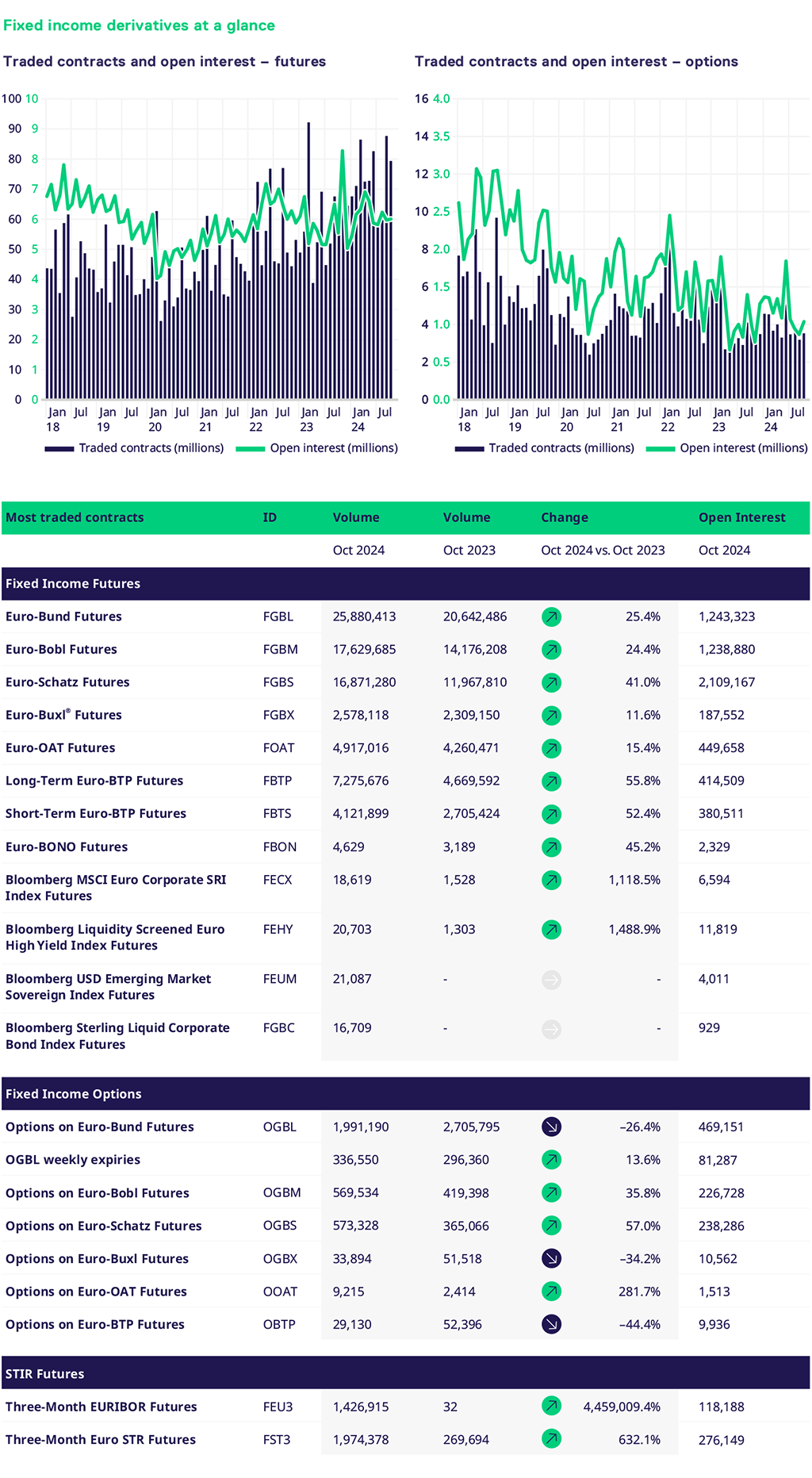

Bund, Bobl and Schatz futures volumes grew by 25%, 24% and 41% respectively, OAT Futures increased by 15%, and the Italian futures, the Long-term and Short-term BTP, continued their upwards trajectory with 55% and 52% volume increases.

On the options front it was more of a mixed result, with Bund options down 26%, while Bobl and Schatz grew 35% and 57%. Bund weekly options have continued to grow throughout 2024, trading 2.5mn contracts so far in 2024. Options on OAT futures continued their revival since the snap French elections in the summer, with 45k contracts traded in 2024.

After a bumper roll-month in September, Credit Index futures were back to business as usual. Euro IG traded 18.6k contracts, Euro High Yield 20.7k, whereas Sterling IG traded 16.7k and USD EM traded 21k. In total over 5.2bn in notional was traded in the Credit Index Futures in October, almost 15 times more than in 2023. The newly launched Bloomberg US Corporate Index Futures and Bloomberg US High Yield Very Liquid Index Futures printed their first trades. The interest in these products we have received from clients in recent events we organized around the launch, reinforces our belief that this asset class has enormous potential.

In STIRs, €STR futures averaged c.86k contracts per day and Euribor 62k. Open interest in €STR futures continued to grow, reaching 276k at the end of the month. Euribor open interest now stands at 118k lots.

The FX segment also showed positive growth in October with a total of c. 162k contracts traded (+45% growth year-on-year). The weak EURUSD led to new hedge transactions, particularly on the buyside, which pushed the OI towards a record high (c. 84k contracts). Outside the G7 area, we are once again seeing increased activity in the Scandinavian currency pairs (especially NOK/SEK) and also in some EM currency pairs such as MXN/USD and ZAR/USD.

|