Apr 08, 2016

Eurex

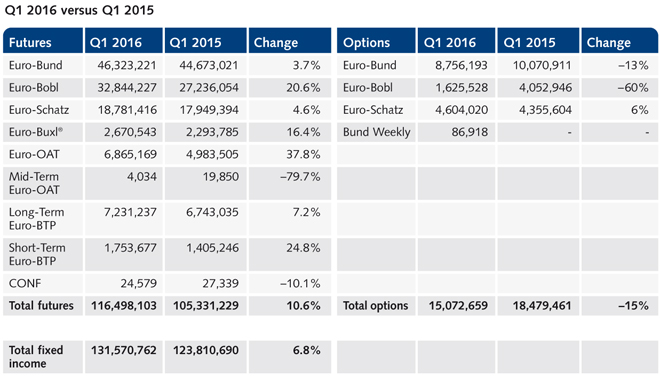

Eurex Exchange's Fixed Income Futures & Options: highlights of Q1/2016

The first quarter of 2016 commenced with high market volatility and a sense of gloom. The fears of deflation and recession were the main source of this pessimism. Moreover, investors also worried about emerging markets and about China in particular. All eyes were fixed on the next move of the European Central Bank (ECB) which delivered another dosage of quantitative easing effective from 16 March in essence decreasing the rates:

- The rate of refinancing operations of the euro system was decreased to 0.00%.

- The interest rate on the marginal lending facility was decreased to -0.25%.

- The interest rate on the deposit facility was cut to -0.40%.

In addition, the monthly purchases under the asset purchase program will be expanded to EUR 80 billion starting in April and a series of four targeted longer-term refinancing operations (TLTRO II) will be launched starting in June 2016.

Fixed income derivatives volumes were restrained by ECB manoeuvres, however figures for Eurex Futures remained robust:

- A total of 132 million Fixed Income Futures and Options were traded in Q1 2016, an increase of 6.8% compared to Q1 2015. Futures volume increased by 10%.

- There was a lack of clear trading trend, as some players chose to move up the curve while others were more active in non-German assets. The Euro-OAT Futures traded 37% more contracts than in Q1 2015 and Short-Term Euro-BTP Futures had higher flows by 25%. In the core market, Euro-Bobl Futures contracts increased by 20% and the Euro-Buxl® Futures contracts by 16%.

Swap futurization: will it happen in 2016 or 2017?

With the advent of mandatory execution and clearing of OTC interest rate swaps, most market participants expect the OTC swap market to undergo major changes.

The clearing of OTC swaps may turn out to be uneconomical or even unavailable for some market players coercing these entities to reassess the advantages of a tailor-made hedge vs. the cost efficiency of a future. Some of these players might then turn to trading government bond futures or swap futures. The exchanges are anticipating this development, and as a result, a number of swap futures contracts have been launched in the recent years. Eurex launched deliverable 2-, 5-, 10- and 30-year Euro-Swap Futures in 2014 and started offering GMEX Constant Maturity Futures in 2015.

There are some open questions, however. One of them is the lack of urgency. The category 2 & 3 clients who would be the target audience (hedge funds, asset managers, pension funds) will not start clearing until 2017. It remains to be seen whether the buy side will move into swap futures this year or whether this trend will appear in 2017.

Eurex Clearing offers a new access model

Eurex Clearing has launched a new membership type that allows buy-side participants to have a direct contractual relationship with the clearinghouse facilitated by a clearing agent. The so called Individual Segregation Account (ISA) Direct is a unique way for buy side clients to meet new regulatory requirements with reduced counterparty risk and strong protection of their assets. For clearing agents, the new service eases the adaptation to the new capital rules as it frees up equity capital currently required for client's business while maintaining existing client relationships. ISA Direct will be available from summer 2016.

Key features of ISA Direct:

- Direct membership of buy side firms at the Clearing House facilitated by a clearing agent.

- The Clearing Agent acts as agent to cover the default fund contribution, default management obligations and optionally certain operations and financing functions.

- ISA Direct Member maintain legal and beneficial ownership of collateral.

Eurex Exchange - The home of the euro yield curve.