Jul 11, 2018

Eurex | Eurex Clearing

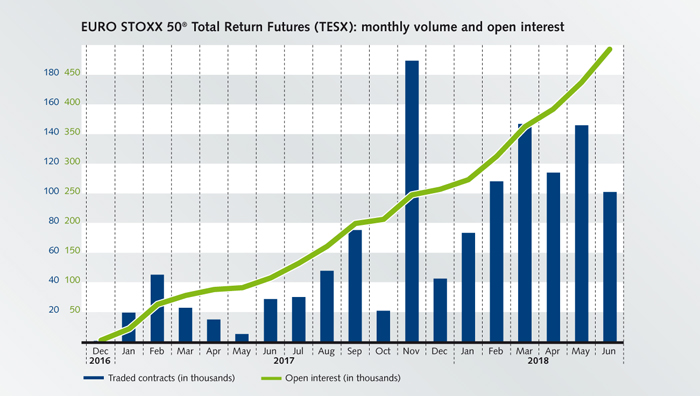

TRF mark open interest record

Open interest in Eurex’ Total Return Futures (TRF) has reached its highest peak to date at 496,000 contracts. This equals roughly EUR 17.0 billion. Average daily volume is now at 5,500 contracts (year-to-date), which translates to EUR 200 million.

“Our product has seen an increase in the repo rate at the front of the curve over the last few months,“ says Stuart Heath from our Product Research & Development team. “The equation is simple, a lower TRF spread means that there is a higher repo rate.” In June, the curve jumped significantly, with TRF spreads turning negative on the September and December expiries. “This means that the repo rate has increased and reverted to positive”, Heath adds. “For the September 2018 expiry this would be a 36 basis points move in a month, for the December 2018 expiry it would be 28.5 basis points.”