Jul 07, 2023

Eurex

Total Return Futures volumes pick up

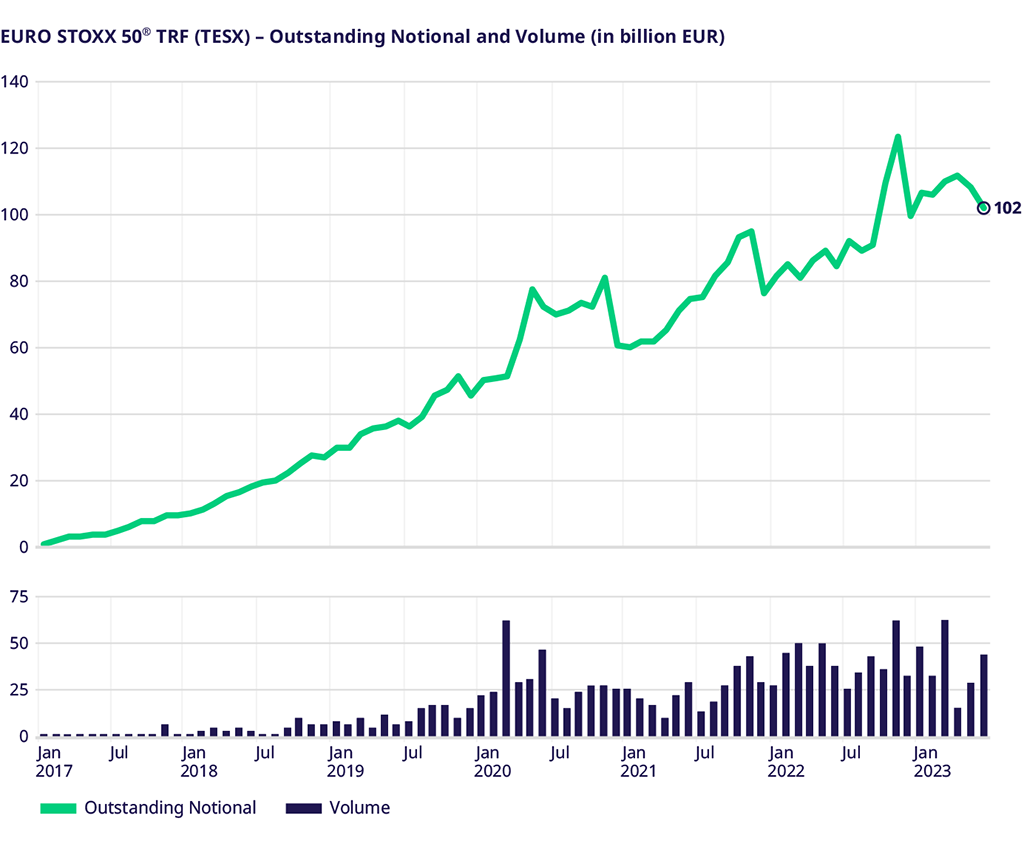

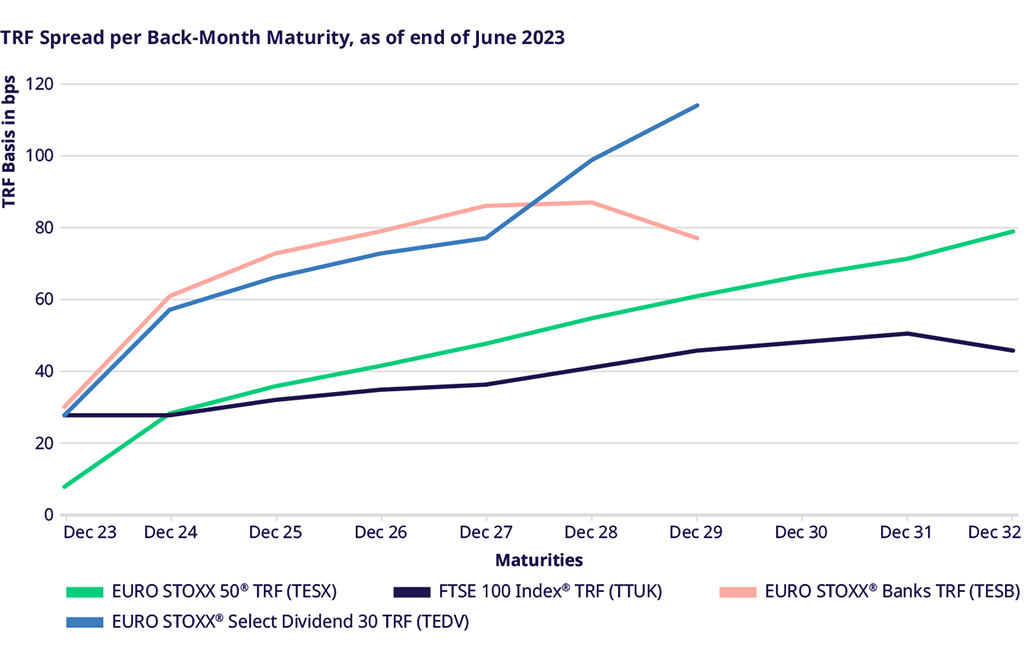

After a lackluster start to Q2, Index Total Return Futures volumes picked up in June. The pick-up had less to do with the usual roll business but more with a shift in market sentiment, combined with a reduction of directional exposure before the summer. This was certainly true for the SX5E, where volumes were up in June and the highest this quarter while overall open interest fell.

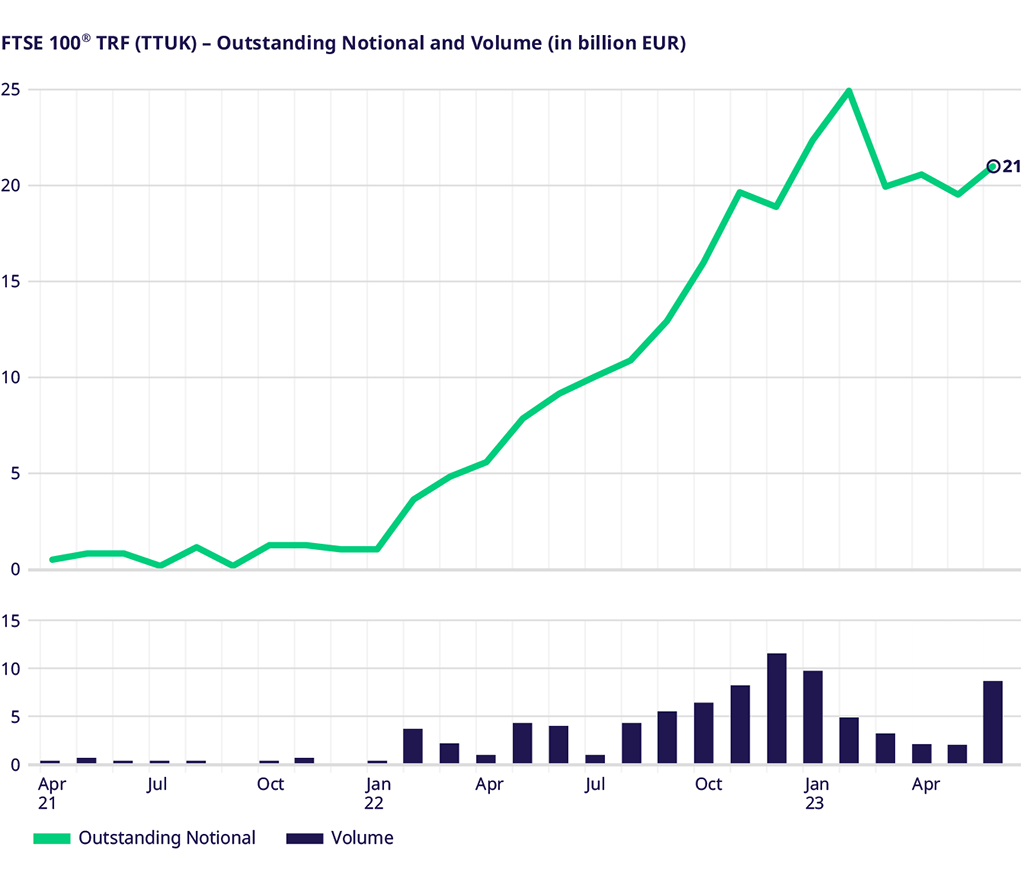

Conversely, we saw the UKX TRF contract increase in open interest on the back of the highest volumes since January, with annual volumes nearly double that of 2022. However, neither of these benchmarks saw any significant change in the curve in terms of traded spreads.

Away from the benchmarks, the Banks sector index, SX7E, continues to grow significantly with overall volumes more than ten times that of 2022 YTD, and the thematic SD3E grew by an even bigger multiple, with June recording an ADV of 1250 contracts.