Jun 15, 2022

Eurex

European benchmark index futures roll update

As we step into the final week of futures roll period, we are showing some statistics of the current June roll with a focus on Benchmark Index Futures.

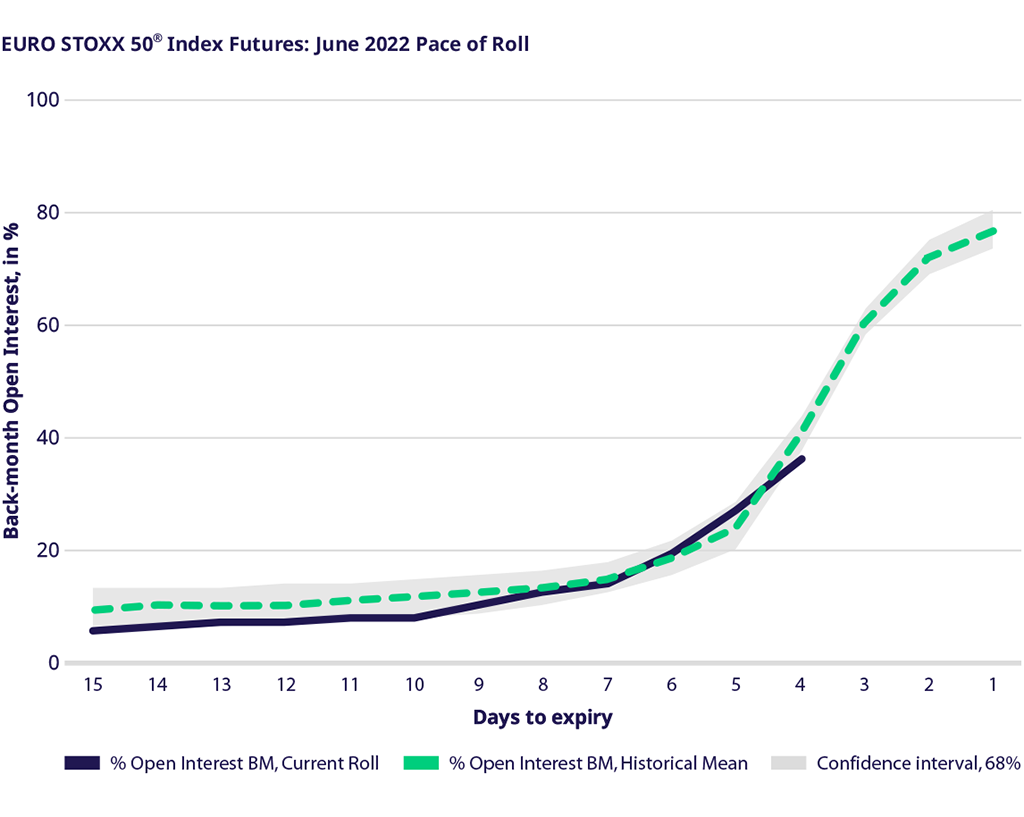

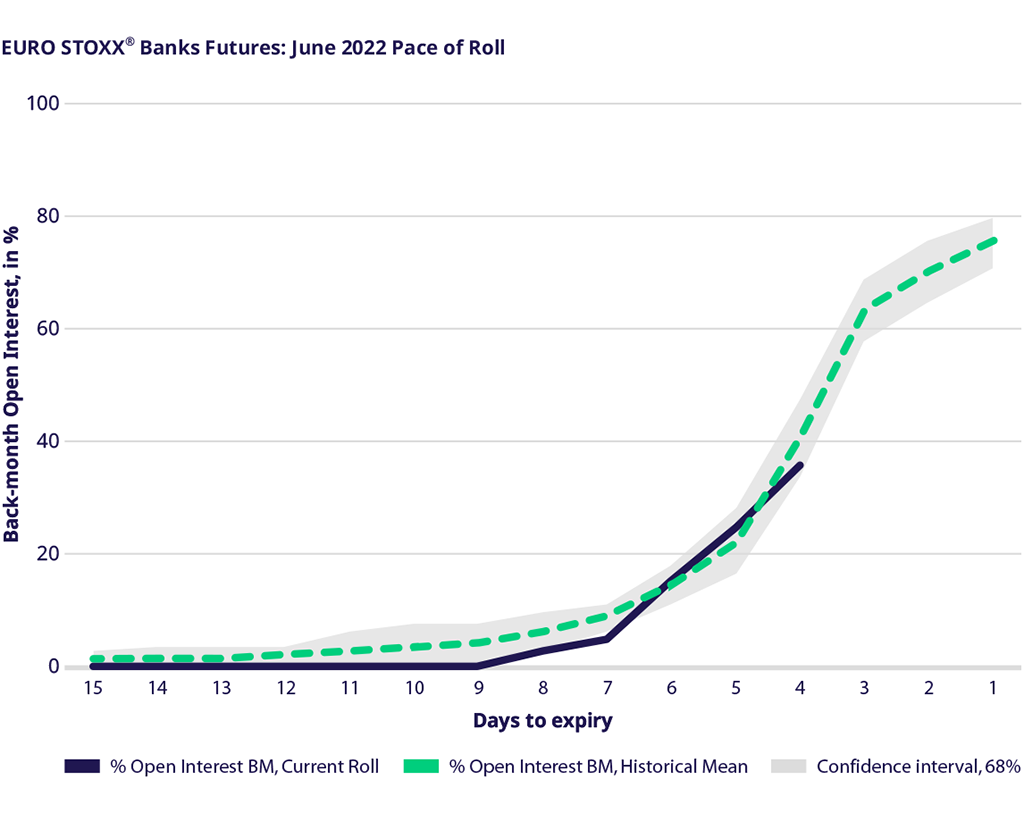

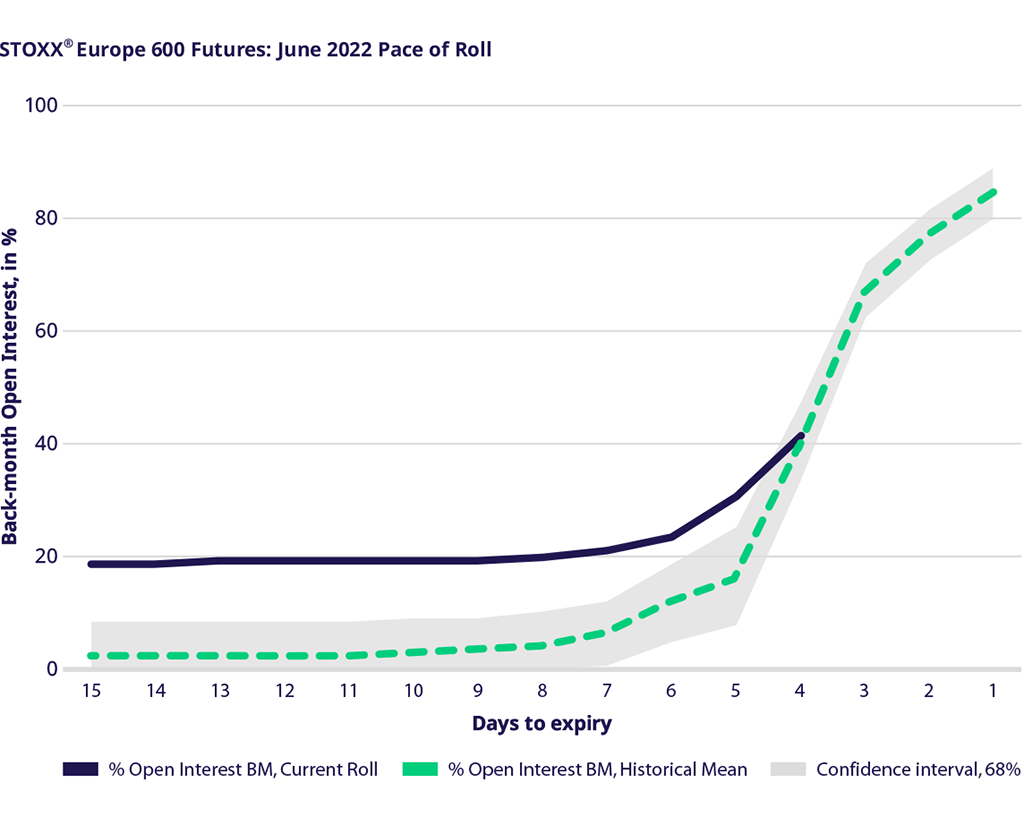

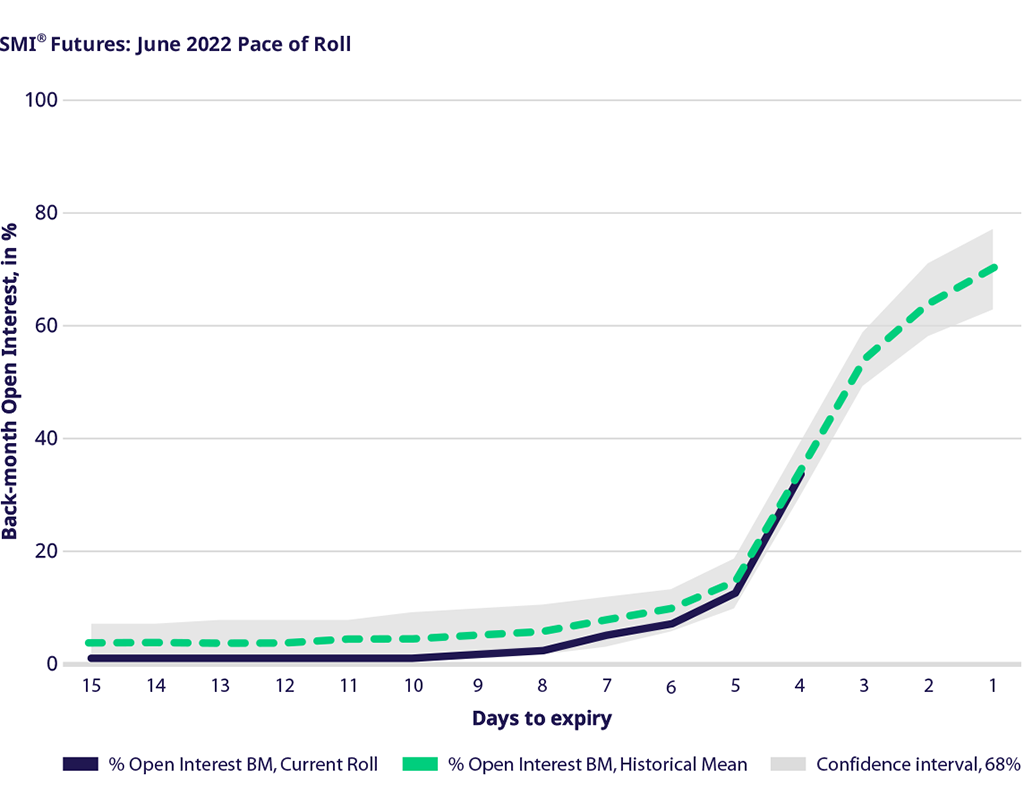

Below, every graph contains a solid line representing the ratio of back month OI to the total OI. The dashed line shows a historical mean of eight recent rolls, while the gray bandwidths depict one standard deviation from the historical mean levels.

The graph shows that the roll started a bit OI underweighted in the back months (5% of total open interest) of the EURO STOXX 50® Index Futures and quickly recovered into the regular rolling track eight trading days before expiry. In the first two weeks of the rolling period, members transferred 35% of OI to the back month. We expect members to roll another 36% of OI in the remaining days before expiry.

This time, members started to roll their positions on EURO STOXX® Banks Futures later than usual, entering back-month expiries just eight days before expiry. On Friday’s market close, we had 22% of open interest accumulated in the back month, with another 53% still expected to be rolled this week.

Unlike the previous times, some members entered the back-month expiry contracts before the start of the rolling period of STOXX® Europe 600 Futures, with their back-month positions roughly at a bay of 20% of total open interest. The rolling activity of other members kicked off seven days before expiry. As of the beginning of this week, 40% of OI was rolled to the back month expiries, resembling the average historical pace of the roll. We expect another 44% of OI to be rolled this week.

SMI® Futures showed smooth rolling activity last week. This week has started with 34% of OI being rolled into the back months, with 35% more to go.