Aug 12, 2015

Eurex Clearing

Byron Baldwin: Cross margining at Eurex Clearing - generating margin, Default Fund & capital efficiencies

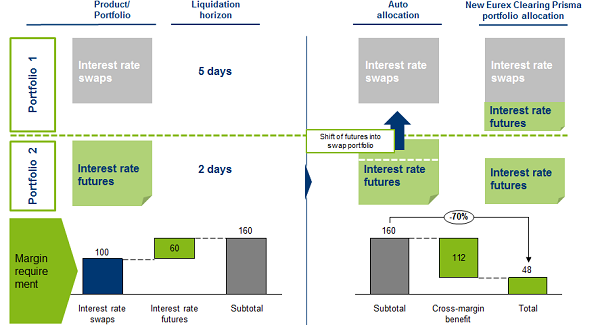

Cross margining at Eurex Clearing is provided by its innovative risk management system Eurex Clearing Prisma (Portfolio RISk MAnagement) which calculates risk and margin on a portfolio basis segmented by pre-defined Liquidation Groups that comprise closely correlated products. The default management is also aligned to products within each Liquidation Group under Eurex Clearing Prisma.

Portfolio-based margining with Eurex Clearing Prisma

For example, the Fixed Income Liquidation Group now comprises over-the-counter interest rate swaps (OTC IRS), Zero Coupon Inflation Swaps (ZCIS) and fixed income and money market futures and options products. From an operational point of view, for the cross margining of a portfolio OTC IRS and exchange-traded derivatives (ETD), there is no physical movement of futures to OTC IRS. The Prisma Margin Optimizer automatically calculates the minimum margin (see diagram below) for a portfolio of OTC IRS and IRS. If there are no offsets between ETD and OTC IRS within the portfolio, margin will default to ETD being margined on a 2 day risk horizon and OTC IRS being margined on a 5 day risk horizon.

Between 62 and 70 percent reduction in initial margin requirements

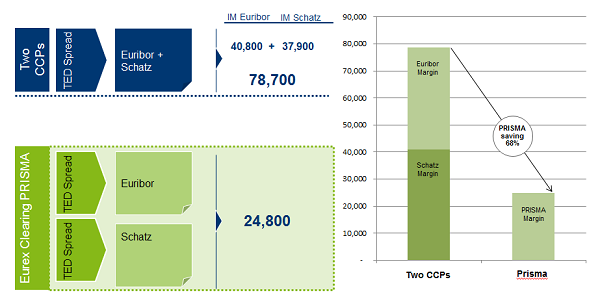

The benefits of cross margining for both the buy side and the sell side can be seen by analyzing the initial margin requirement of a relative value, DV01 neutral, EURIBOR strip versus Euro-Schatz Futures, or 'Term TED' trade. Clearing both products through Eurex Clearing and generating cross margining savings results in a 68 percent reduction in initial margin requirements compared to clearing both products on two separate CCPs.

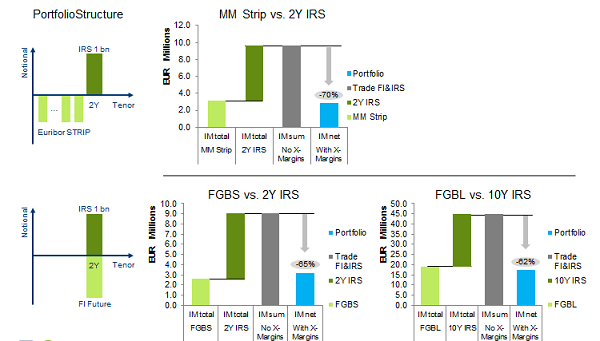

Similarly, cross margining benefits for the sell side and buy side between euro listed derivative products and euro OTC IRS can be seen by analyzing EURIBOR strips or fixed income futures versus euro OTC IRS - euro asset swaps or invoice spreads (see below). Synthetic asset swaps can be created using swap futures and bond futures with similar cross margining benefits.

Cross margining savings generated were between 62 percent and 70 percent, depending on the maturity of the asset swap, compared to clearing both products on separate CCPs. The additional benefit for the sell side is the reduced capital regulatory requirements due to the netting of exposures.

What generates the highest cross margin savings for the buy side and sell side?

Cross currency or cross product margining?

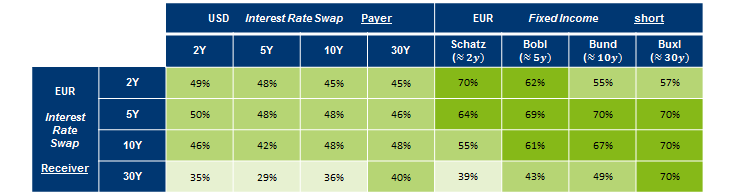

The analysis below of the various cross currency margin savings of various tenors between USD payer OTC IRS and EUR receiver OTC IRS and that of cross product margin savings between various tenor EUR receiver OTC IRS and Eurex Exchange's Euro-Schatz, Bobl, Bund and Buxl® fixed income futures clearly show that cross product cross margin savings far outweigh that of cross currency cross margin savings.

Clearing of EURIBOR, fixed income futures and OTC IRS

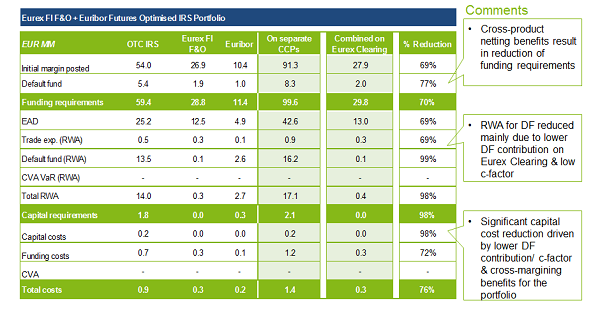

In the new capital constrained world of Basel III, Leverage Ratio and RWA, there are significant benefits for the sell side of clearing EURIBOR, euro fixed income futures and euro OTC IRS through one CCP. An analysis (see below) was carried out of a euro OTC IRS portfolio fully hedged with EURIBOR and Eurex fixed income futures comparing initial margin, Default Fund contribution, EAD, RWA and capital and funding costs to clearing all three products through Eurex Clearing to that of clearing through three separate CCPs. The analysis showed that, by clearing all three products through Eurex Clearing, the sell side benefitted from a 69 percent reduction in initial margin requirements, a 77 percent reduction in Default Fund contributions, a 69 percent reduction in TE RWA and a 72 percent reduction in funding costs.

ZCIS, the latest addition to the Fixed Income Liquidation Group

On 3 August, EurexOTC Clear expanded its OTC IRS product list with the launch of the clearing of Zero-Coupon Inflation Swaps (ZCIS) for the Euro Consumer Price Index, HICPxT, French Consumer Price Index, FRCPIx, and the UK Retail Price Index, UKRPI.

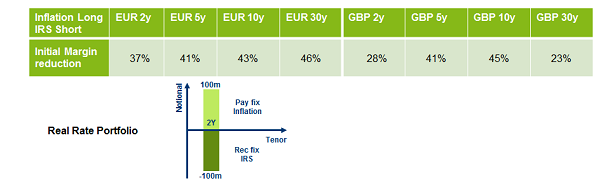

ZCIS will be cleared within the the Fixed Income Liquidation Group with OTC IRS and fixed income and money market futures and options giving the buy side and sell side alike superior portfolio margining benefits compared to a silo'd CCP IRS offering across the three asset classes of OTC IRS, ZCIS and Euro listed derivative products. Below are examples of the initial margin savings of EUR and GBP real rate portfolios of various tenors of ZCIS and OTC IRS.

Conclusion

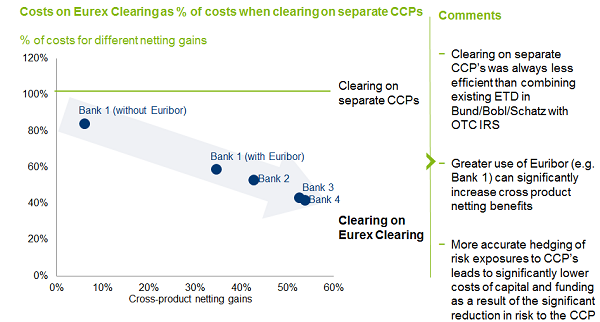

In conclusion, 'the proof is in the pudding' - four actual Banks' proprietary euro fixed income futures and euro OTC IRS portfolios were analyzed, comparing the costs of clearing euro listed derivative products and OTC IRS on separate CCPs to that of clearing all products on Eurex Clearing. For one bank the analysis was carried out in two scenarios, 1) without EURIBOR and 2) with EURIBOR).

The analysis by Oliver Wyman (see below) showed that by clearing all euro-listed derivative products and OTC IRS through Eurex Clearing generated between 40 percent and 59 percent cost savings for the sell side in terms of lower initial margin requirements, lower Default Fund contributions and lower capital regulatory requirements through the netting of exposures.

Byron Baldwin, Senior Vice President, OTC Clearing at Eurex Clearing, London.