Oct 30, 2017

Eurex Clearing

Part 3: Initial margin trends and stress testing

Pioneering CCP Transparency Series

The Public Quantitative Disclosure (PQD) is an internationally agreed format defined by CPMI-IOSCO with the intention of enhancing CCP market transparency. Eurex Clearing has been publishing its PQD since 2015 and continues to strongly support CCP transparency and market stability.

With the disclosure of Q4/2016, Eurex Clearing began a series of commentary to highlight key trends, discuss current topics and shed some light on selected data points. The current note is the third part of the series and contains key highlights for the second quarter of 2017.

Initial and variation margin

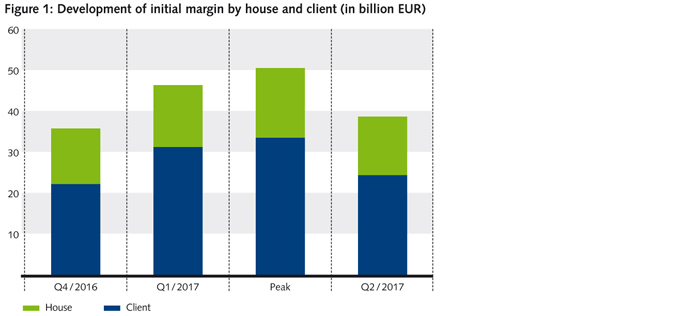

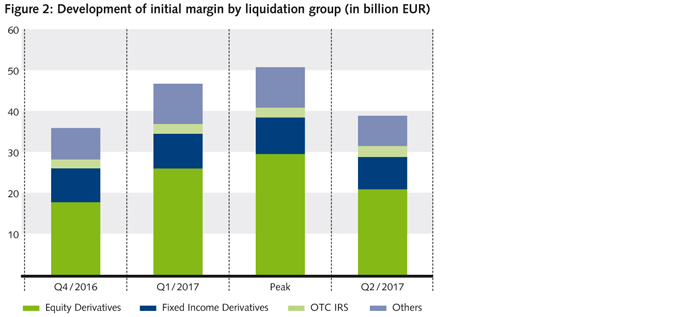

Since end of Q1 2017, initial margin requirements have further increased by almost 10% to more than EUR 50bn until the French presidential election in May 2017, constituting the highest initial margin level since September 2015. After the French presidential election, the initial margins decreased back to about last year’s levels. Initial margins are mainly driven by client exposures (about 60% of overall margin requirement) in equity derivatives (about EUR 20.4bn), fixed income derivatives (about EUR 7.9bn) and OTC IRS contracts (about EUR 2.8bn).

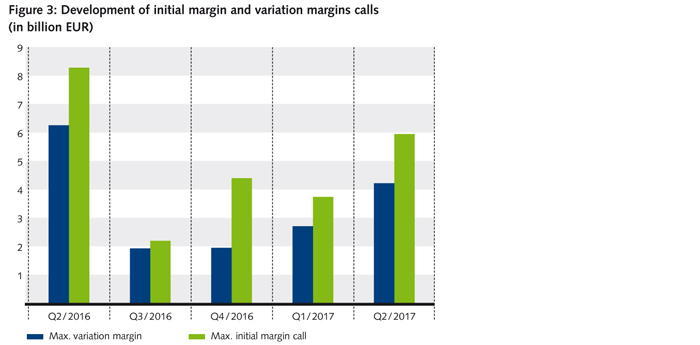

In line with the overall larger cleared volumes and initial margins during Q2 2017, the maximum daily variation margin (up to EUR 4.3bn (PQD 6_7_1)) and daily aggregate initial margin call1 (up to EUR 6.0bn (PQD 6_8_1)) levels increased. Nevertheless the respective levels around the Brexit referendum in 2016, with a maximum variation margin of EUR 6.3bn (PQD Q2/2016 6_7_1) and daily initial margin call of EUR 8.3bn (PQD Q3/2016 6_8_1) have not been reached.

Credit stress testing

Testing member portfolios under extreme but plausible scenarios yields valuable insights into potential losses beyond margins. Stress test results are used for the sizing of the CCP’s Default Fund, a significant element in CCP financial resources and hence ultimately ensure the safety of the clearing business.

The PQD provides information on the value of required pre-funded default resources (excluding initial margin) (PQD 4_1_4), whether a CCP is subject to a cover-1 or cover-2 requirement (PQD 4_4_1), the assumed holding period (PQD 4_4_2), the estimated largest aggregate stress loss (in excess of initial margin) (PQD 4_4_3 and 4_4_7). In addition, metrics on the severity and duration in case the coverage requirement was exceeded (PQD 4_4_4 , 4_4_5, 4_4_8, 4_4_9) are provided.

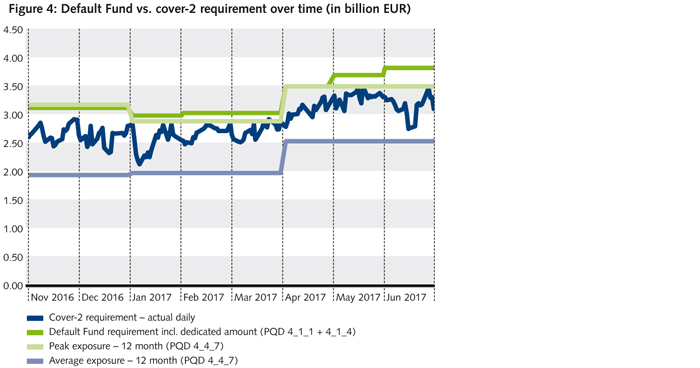

Due to increasing volumes in Eurex Clearing’s benchmark products in Q2 2017 the cover-2 requirement did also increase. Figure 1 shows a comparison between cover-2 requirement (based on both PQD 4_4_7 trailing peak and mean 12 month values and actual daily computed numbers) and Default Fund requirement2 (PQD 4_1_1), including the dedicated amount (PQD 4_1_4). We include the actual daily values for the cover-2 requirement to provide more transparency and as the average and peak values shown in the PQD are not readily comparable with the actual Default Fund size.

Key points to consider while interpreting the stress testing numbers:3

• The adequacy of the Default Fund is monitored daily based on the results of the cover-2 stress test scenario (compare the dark blue and green lines in Figure 4 above)

• Eurex Clearing defines the cover-2 at the level of company groups (including affiliates and all clients)4 with the largest losses over all stress testing scenarios during the holding period. Client positions can be a key driver (see Figure 1) under assumption that no porting of client positions is performed (independent of the segregation model). This is a conservative assumptions, required by EMIR and in line with the CPMI-IOSCO guidance on resilience of CCPs

• Eurex Clearing assumes that the two company groups default within the holding period of several days under different market scenarios (e.g. one member may default during a market event, which causes falling stock prices, and the other one during a market rebound when stock prices are rising again)

• The netting logic used to calculate the stress results on a company level respects segregation rules, which do not allow to offset segregated client gains with proprietary losses, but permit that client losses are offset with proprietary gains

• Any collateral posted in excess of the margin and Default Fund requirement (i.e. overcollateralization), is not considered in the stress shortage calculation, assuming that overcollateralization may be withdrawn by participants.

1 Please note that the aggregated figure also includes intraday variation margin calls.

2 Eurex Clearing’s Default Fund size is recalibrated on a monthly basis in order to reflect changing market conditions. Intra-month mitigating actions can be taken to ensure that a certain minimum buffer above the cover-2 requirement is always maintained.

3 More details on Eurex Clearing’s stress testing framework are available here: http://www.eurexclearing.com/clearing-en/risk-management/stress-testing

4 Please note, that the company group and its affiliate are assumed to be in default under the same market scenario