Aug 12, 2014

Eurex Clearing

Cross margining at Eurex Clearing, part 2

The development of clearing for OTC products in 2012 brought with it a more sophisticated approach to margin calculation, in particular Value at Risk (VaR). The need for VaR is driven by the long term nature of OTC products, with interest rate swaps reaching out to 50 year terms, potentially making a portfolio more reactive to market conditions and margin requirements than the ETD market going out to around two years.

While the older method, the SPAN-like Risk-Based-Margining (RBM) for the listed world was appropriate to calculate ETD exposure, it is no longer sufficient enough to deal with OTC IRS risk. As a consequence, Eurex Clearing decided to introduce a new VaR-based approach and ultimately to use it for all asset classes under the Eurex Clearing umbrella. This was the decision leading to a consolidated margin calculation method, providing a unique approach across product classes and offering margin offsets where there had not been any in the past.

VaR is a statistical method with alternative approaches to practical implementation. The most popular approach is that of Historical Simulation, where the prior history of the market is used to simulate the behaviour of the current portfolio of trades to derive the outcome of market scenarios. With these portfolio simulation scenarios, a CCP then has choices in how to select the amount of margin, one being Worst Case Loss (WCL), another being Expected Shortfall.

In order to end up with the most sophisticated and advanced risk calculation method on the market, the Prisma VaR model takes into account multiple factors to calculate margin for a portfolio including:

- 750 filtered historical scenarios

- 250 un-filtered stress scenarios

- Adjustment for correlation breaks and model error

- Adjustment for liquidity along the yield curve

- Adjustment for expiry risk

Combining OTC and ETD into a single margin model

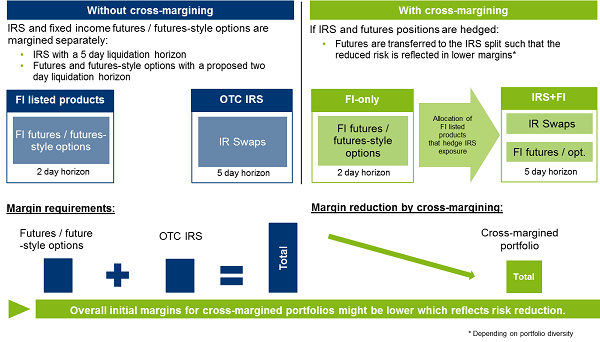

There are a number of considerations in combining OTC and ETD products into a single margin calculation including the calculation method and the holding period (or Margin Period of Risk).

In a pure OTC portfolio, Eurex Clearing uses a five day holding period in the VaR calculation which is driven by regulatory standards and allows for the auction process of a defaulted member. In the ETD market, two days is the typical holding period for interest rate products, as selling or liquidating futures and options positions can be achieved quickly in a liquid market via the electronic order books.

When including ETD products into a combined cross margin calculation, Eurex Clearing treats those ETD products with a five day holding period, which act as a hedge against IRS trades. As a result, the overall exposure consists of a combined IRS+ETD sub-portfolio (calculated with five-day holding period) and those ETD positions which do not act as hedging trades to IRS exposure (correspondingly only calculated with two-day holding period).

In order to offer clearing members the maximum margin benefit, the described process takes place completely automatically every two hours during business. Hereby market participants, active both in ETD and OTC, are able to feel certain that intraday trading and clearing activity always leads to the maximum cross product margin offsetting effect without lifting a finger.

One fundamental principle that Eurex Clearing has adopted, is that combining OTC and ETD positions must actually reduce the initial margin level, otherwise the hedge allocation would not be applied.

Transparency is granted by extensive reporting and the possibility for all market participants to fully integrate the algorithms into their in-house infrastructure.

Product coverage within the OTC and ETD Liquidation Group

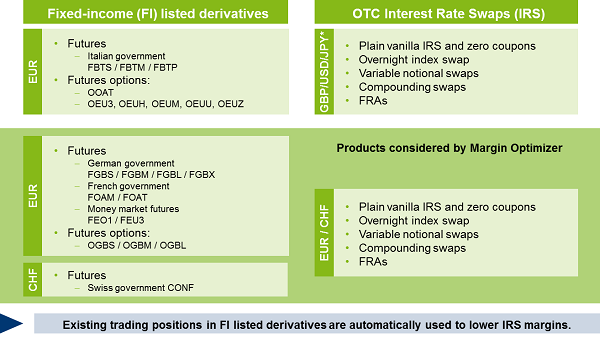

The combined OTC and ETD liquidation group can contain multiple products, intended to allow offsets in the short, medium and long term maturities covered by the ETD market. In the OTC market, the Eurex Clearing platform allows for a wide range of interest rate products and has considerable support from the sell and buy-side.

Next to all the fixed income products available for trading and clearing at Eurex Group, there is currently a large subset of products eligible for cross margining. Clearing members can facilitate options and futures on Bund, Bobl, Schatz and Buxl, the money market futures, French and Swiss government futures to hedge OTC exposure in IRS, FRAs and zero coupons, overnight index swaps, variable notional and compounding swaps.

Eurex Clearing is naturally positioned as the hub for EUR-denominated products, OTC and ETD alike.

Hedge ratios

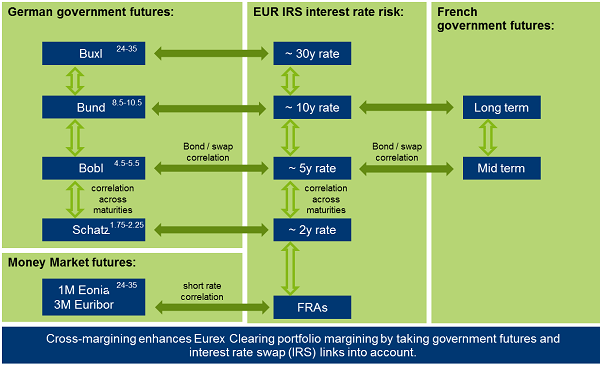

Eurex has implemented a position matching algorithm in Prisma which uses the DV01 sensitivity of ETD products to discover if their inclusion achieves a minimum level of margin reduction. This is automatically checked for all maturity buckets of clients’ portfolios.

Obviously the Bund future is an appropriate hedge position against a 10y interest rate swap but one shorter or one longer ETD product can serve for a cross margin reduction as well. That would be a Bobl or a Buxl in the Bund example which would create an offsetting effect, even when the hedge ratio is not that big compared to the Bund.

Practical considerations

The described process happens automatically at Eurex Clearing. There is no need for clearing members or clients to manually transfer positions between accounts to increase the offsetting effect. The only prerequisites for cross margining on clients’ side are, that the respective ETD positions were migrated to Prisma, the cross margining functionality was switched on in the migration process and that all ETD and OTC trades are cleared in the same virtual position account (under the same segregation model).

Further effects on members’ back-office procedures are obviously the reporting and reconciliation efforts to distinguish between ETD, OTC and combined risk exposures. In order to make this as smooth and transparent as possible, Eurex Clearing introduced new reports providing the full picture on cleared positions and risk figures.

Furthermore Eurex Clearing is in close contact to major vendors, both on the listed and OTC side, to jointly work on suitable back-office risk and position management suites which are as well able to replicate the cross margining algorithm. There is no question that this has a major impact on members’ internal processes and system infrastructure. Therefore, the move to cross margining is nothing that should be considered as overly quick and straightforward. The move on clearing house level is as easy as it gets but depending on the level of IT-integration and back-office functions on clearing members’ side this could lead to a larger process of change.

This is the second part of a 3 part series. For part 1 please refer to our "Further information" section.

(First published by The OTC Space)